Home › Market News › Interest Rates, Inflation, and Fresh Market Performance Summaries

The Economic Calendar:

MONDAY: Empire State Manufacturing Index, Patrick Harker Speaks, 3-Month Bill Auction, 6-Month Bill Auction, Patrick Harker Speaks

TUESDAY: John Williams Speaks, Retail Sales, Industrial Production, Michelle Bowman Speaks, Business Inventories, Housing Market Index, Tom Barkin Speaks

WEDNESDAY: MBA Mortgage Applications, Housing Starts and Permits, EIA Petroleum Status Report, 4-Month Bill Auction, Christopher Waller Speaks, John Williams Speaks, Michelle Bowman Speaks, 20-Yr Bond Auction, Beige Book, Patrick Harker Speaks, Treasury International Capital, Lisa Cook Speaks

THURSDAY: Jobless Claims, Philadelphia Fed Manufacturing Index, Philip Jefferson Speaks, Existing Home Sales, Leading Indicators, EIA Natural Gas Report, 4-Week Bill Auction, 8-Week Bill Auction, Jerome Powell Speaks, 5-Yr TIPS Auction, Austan Goolsbee Speaks, Michael Barr Speaks, Raphael Bostic Speaks, Fed Balance Sheet, Patrick Harker Speaks

FRIDAY: Patrick Harker Speaks, Loretta Mester Speaks, Baker Hughes Rig Count

Key Events:

The developing conflict between Israel/Gaza has traders punting into risk-off trades and downside stock market hedges.

Stocks wrapped the week with mixed results after large U.S. banks kicked off earnings season with upbeat reports that beat expectations. The S&P 500 was higher +0.24%, and the Nasdaq-100 dropped -0.04%.

Traders will focus on earnings season, the geopolitical conflict, and UAW strikes over the next few weeks.

Here are a few interesting quotes from bank CEO’s:

JPM CEO Jamie Dimon said: “Currently, U.S. consumers and businesses generally remain healthy, although consumers are spending down their excess cash buffers.”

Blackrock CEO Larry Fink said, “For the first time in nearly two decades, clients are earning a real return in cash and can wait for more policy and market certainty before re-risking.”

We flipped on the ‘higher-for-longer’ call last week. The simple reason is that it is now the consensus trade. We feel that outsized returns come from not going with the herd. So far, it was a good call as 10-year treasury note futures traded higher.

The U.S. rate selloff has been driven by three fundamental factors: (1) robust US data, (2)

daunting supply/demand imbalance, and (3) challenged asset manager positioning. The September FOMC meeting exacerbated the move.

It’s hard to see how the September CPI changes and FOMC member’s minds on rates decisions, including the November Fed decision.

The Fed Funds futures market is pricing a 91% on no rate change at the November meeting.

Source: CME Fedwatch

In global oil dynamics, recent developments have briefly alleviated the so-called “war premium” traditionally associated with geopolitical tensions. This shift was instigated by Saudi Arabia’s reassurances that their oil production would remain undisturbed, ensuring an unhampered supply chain.

It’s noteworthy that, as of now, the supply landscape remains unscathed. The Kingdom of Saudi Arabia further conveyed its willingness to accommodate any interested parties seeking to procure their oil. Concurrently, in collaboration with Russia, they opted to extend production cuts through the year’s end, with potential extensions into the new year.

In the intricate tapestry of oil trading, market participants had factored in a premium of approximately $4, primarily in response to the Israel/Hamas conflict. This climactic price at the moment, often referred to as the “Scene of the Crime,” revolved around the West Texas Intermediate (WTI) price level of roughly $83. Notably, this market segment experienced a reconfiguration mid-week back down around $82.5, culminating at the week’s close at $87.65.

Meanwhile, President Biden has issued cautionary remarks to Iran on the international stage, suggesting they tread carefully. Nevertheless, the implementation of oil-related sanctions against Iran remains uncertain. In stark contrast, the Biden administration has persistently enforced measures targeting the U.S. shale industry, deploying an array of legal actions and executive directives.

CPI is still printing hot, but It’s hard to see how the September CPI changes anybody’s mind about the November Fed decision.

The good news is that core inflation has slowed markedly beginning in June. The bad news is that the latest data highlight the risk that inflation settles out at 3% and not 2%.

Long U.S. dollar futures and short interest rate futures (long yield) are the most crowded trades, according to a recent survey from BofA.

Source: BofA Research

Federal Reserve policymakers agreed last month that interest rates must remain elevated for some time to bring inflation down to their 2% target. However, they also acknowledged the risk of overtightening monetary policy and causing a recession.

The latest minutes from the Fed’s September meeting, released on Wednesday, revealed little new information about the central bank’s plans for interest rates. However, they did confirm that policymakers are committed to keeping monetary policy restrictive until inflation is under control.

This is likely to mean that the Fed will continue to raise interest rates at its next few meetings and remain high for some time. This could hurt economic growth, but it is necessary to bring inflation down to sustainable levels.

Markets reacted minimally to the latest minutes, as they were largely in line with expectations. However, investors will be closely watching the Fed’s next meeting in November for further clues about the central bank’s plans for interest rates.

Crude oil futures are back above the 10-day moving average as it appears that Israel is ready to move on the Gaza Strip, and Iran threatens a new front of terror against Israel.

The risk of a larger response by Israel and its allies will happen anytime. We believe it’s not a matter of whether it will happen but when.

The UN says Israel has ordered the evacuation of 1.1 million people from the northern part of Gaza.

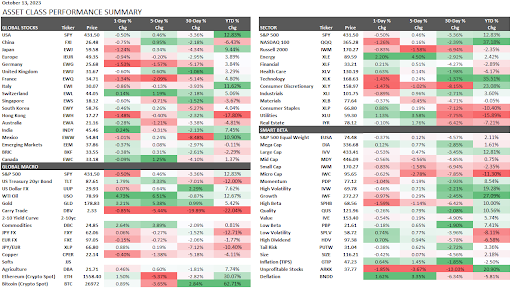

These performance charts track the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.