Home › Market News › Consumer Confidence, GDP, and Another Rate Hike In Sight

The Economic Calendar:

MONDAY: Chicago Fed National Activity Index, Dallas Fed Manufacturing Survey, 3-Month Bill Auction, 6-Month Bill Auction

TUESDAY: Case-Shiller Home Price Index, FHFA House Price Index, Consumer Confidence, New Home Sales, Richmond Fed Manufacturing Index, 2-Yr Note Auction, Money Supply

WEDNESDAY: MBA Mortgage Applications, Durable Goods Orders, International Trade in Goods, Retail Inventories, Wholesale Inventories, State Street Investor Confidence Index, EIA Petroleum Status Report, Survey of Business Uncertainty, 4-Month Bill Auction, 2-Yr FRN Note Auction, 5-Yr Note Auction

THURSDAY: GDP, Jobless Claims, Pending Home Sales Index, EIA Natural Gas Report, Kansas City Fed Manufacturing Index, 4-Week Bill Auction, 8-Week Bill Auction, 7-Yr Note Auction, Fed Balance Sheet

FRIDAY: Personal Income and Outlays, Employment Cost Index, Chicago PMI, Consumer Sentiment, Baker Hughes Rig Count, Farm Prices

Futures Expiration and Rolls This Week:

There are no expiration or rolls this week

Key Events:

| MOST TRADED PRODUCTS | WINNING TRADE PERCENTAGE | AVG. WINNING TRADE | AVG. WINNING TRADE DURATION |

| E-Mini Nasdaq 100 (NQ) | NQ: 53.8% | NQ: $197.17 | NQ: 20.97 Minutes |

| E-Mini S&P 500 (ES) | ES: 44.4% | ES: $237.19 | ES: 32.49 Minutes |

| Micro E-Mini Nasdaq 100 (MNQ) | MNQ: 47.2% | MNQ: $35.19 | MNQ: 79.33 Minutes |

Stock indexes were slightly down on the week. The S&P 500 fell -0.06% for the week, and the Nasdaq index was lower by -0.62%.

A recent pattern has emerged in the prices of ES futures in the overnight trading session. This is a marked change from most of the last decade. The difference is that more and more of the S&P 500’s movement is happening in the overnight futures sessions.

Lately, we have seen many gap-down prices in the overnight session. Then, when regular trading hours start, traders bid stocks up after macro traders sold futures down overnight.

In the last four weeks, SPX is +4.7% cumulatively (+0.2%/day) from cash open to close.

A few key short-term levels for the S&P 500:

Upside: 4208,4220,4230,4265

Downside: 4130,4095,4083,4060

The market expects the Fed to shift into a “rates on hold” stance after the May FOMC meeting.

Last week’s Fedspeak further confirmed market expectations for another 25 basis point rate hike at the May 2-3 FOMC meeting. However, there is disagreement over rate expectations beyond the May meeting.

FEDSPEAK:

-Chicago Fed President Gooslebee said he still needed to decide about the May meeting. However, he stressed that the Fed should “be prudent and patient.”

-Cleveland Fed President Mester stated last week that the Fed “needs to be prudent in assessing all of the incoming economic and financial information.” Although she supported a 25bp rate hike at the May meeting, Mester seemed to be in the camp of “one more hike and a pause.”

-The most hawkish St. Louis Fed President Bullard continued to downplay the impact of the SVB/Signature Bank incidents and raised the possibility of the current rate hiking cycle continuing into autumn. Note that Bullard’s dot at the March FOMC meeting was 5.625%. That suggests three more 25bp rate hikes (in May, June, and July) are his base case.

U.S. Treasury yields compared to the last newsletter:

30-Year yield 3.77% vs. 3.73%

10-Year yield 3.57% vs. 3.51%

5-Year yield 3.66% vs. 3.60%

2-Year yield 4.18% vs. 4.10%

2-10 Yield spread -0.61 vs. -0.58

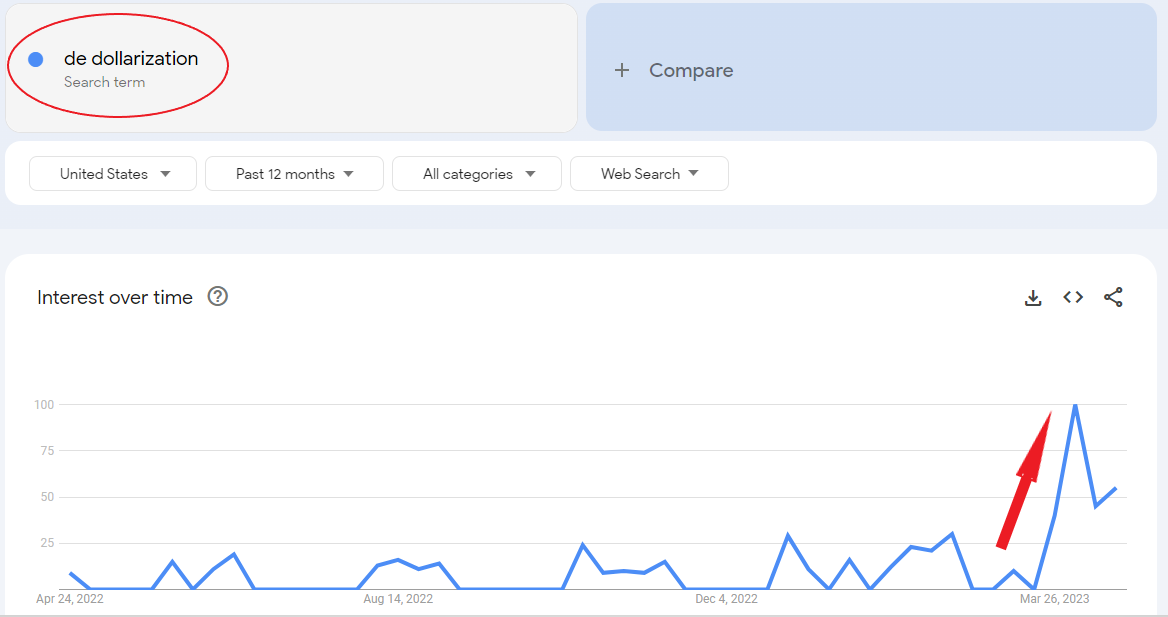

There is a massive increase in media interest in “De-Dollarization.” Note the trend in Google search for the term in the graph below.

The media has expressed concerns about the USD losing its reserve currency status in years past. Is this time different?

In past U.S. dollar down cycles, most of the decline in the Dollar was attributed to investment behavior in a world of ultra-low yields. Traders and investors would reach for higher returns in other currencies like the AUD, CAD, and CNY.

Recently, some of the Dollar’s decline can be attributed to normal market forces as Treasuries fell and Asian central banks sold their Dollar holdings. Some of this was to counter the stronger Dollar last year.

The narrative is also picking up on speculation about more commodity transactions using CNY as the transactional currency and the fallout from the U.S. seizing Russian reserves as a sanction from the Ukraine-Russia war.

China is not ready for the CNY to be the world’s reserve currency. There are several hurdles to attaining the top status of the global transaction currency, including the trust of the capital markets, open trade, free markets, payment options, and regulatory framework. China still needs to sway many countries to take the existing risks.

The Middle East, China, and India are buying record amounts of Russian crude oil. In Europe and the U.S., they are knowingly buying laundered Russian oil in a refined format that is helping finance the Russian war with Ukraine.

Reports show that China, Turkey, the UAE, Singapore, India, Saudi Arabia, and other countries have feasted on Russian crude oil. Now some of those countries have refined that oil, and they’re selling it back to the E.U., Australia, and other G7 nations in product form.

Forbes says that countries are laundering Russian oil. They quote the Centre for Research on Energy and Clean Air (CREA ) saying that China, India, the United Arab Emirates, Turkey, and Singapore as “laundromat countries” that increased imports of Russian oil after the Ukraine invasion.

Bitcoin backed away somewhat from the USD 30k level last week. Bitcoin is currently trading at around $27.5k.

BTC is still up 65% since the start of 2023, in a rally driven by speculation that the Federal Reserve will soon capitulate and the recent stresses in the global banking system that sparked investor interest in alternative assets. It’s down 34.3% from a year ago, though, amid the fallout of high-profile failures and increased regulatory scrutiny.

The Bank of Japan will conduct its first policy meeting under the newly appointed leadership of Governor Ueda. The central bank is expected to maintain current monetary policy settings of rates at -0.10% and QQE with YCC to flexibly target 10yr JGB yields at 0% within a +/- 50bps tolerance range.

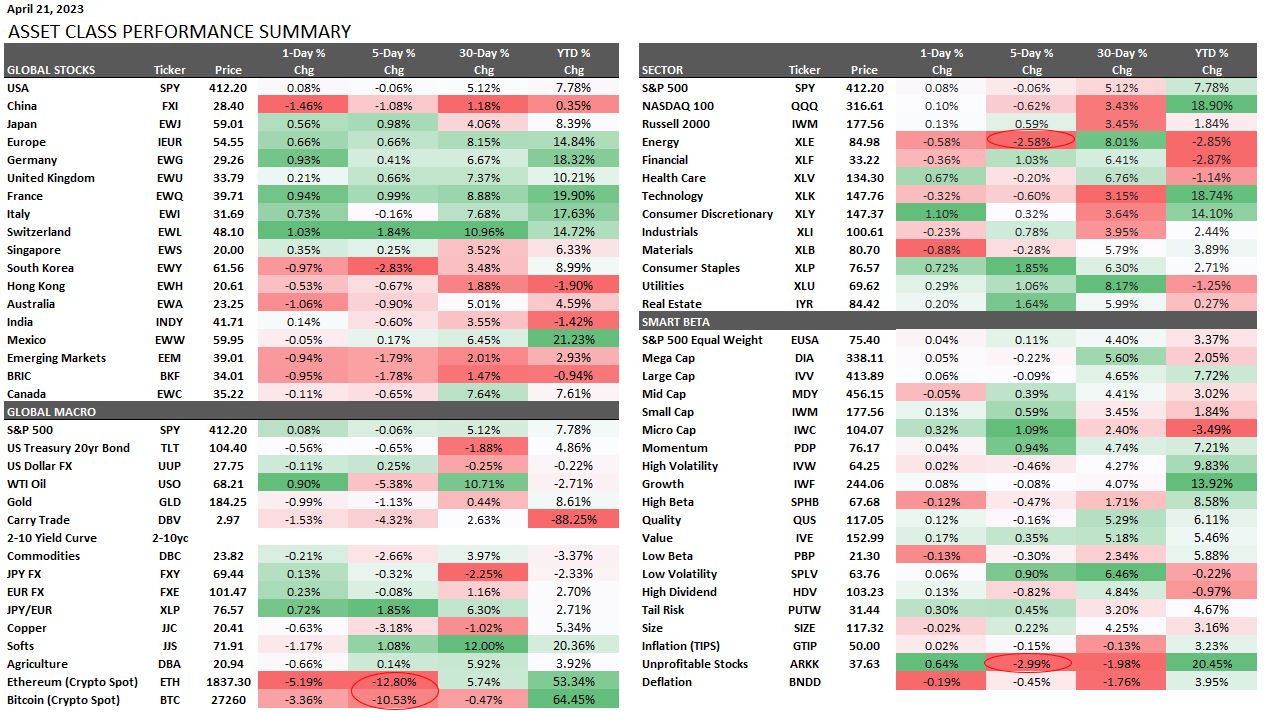

This performance chart tracks the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.

One of the main lessons I was taught as a junior trader is that by 7 am Monday, you should clearly understand all the major things happening in global markets in the coming week. BE PREPARED!