Home › Market News › The Debt Ceiling, Grain Futures, and More Fed Talk

The Economic Calendar:

MONDAY: James Bullard Speaks, Thomas Barkin Speaks, Mary Daly Speaks, 3-Month Bill Auction, 6-Month Bill Auction

TUESDAY: Lorrie Logan Speaks, PMI Composite Flash, New Home Sales, Richmond Fed Manufacturing Index, 2-Yr Note Auction, Money Supply

WEDNESDAY: MBA Mortgage Applications, State Street Investor Confidence Index, EIA Petroleum Status Report, Survey of Business Uncertainty, 4-Month Bill Auction, 2-Yr FRN Note Auction, 5-Yr Note Auction, FOMC Minutes

THURSDAY: GDP, Jobless Claims, Chicago Fed National Activity Index, Corporate Profits, Pending Home Sales Index, EIA Natural Gas Report, Susan Collins Speaks, Kansas City Fed Manufacturing Index, 4-Week Bill Auction, 8-Week Bill Auction, 7-Yr Note Auction, Fed Balance Sheet

FRIDAY: Durable Goods Orders, International Trade in Goods, Personal Income and Outlays, Retail Inventories, Wholesale Inventories, Consumer Sentiment, Baker Hughes Rig Count

Futures Expiration and Rolls This Week:

Monday, May 22nd is the last trading day for June (M) Crude Oil Futures

Key Events:

Stock indexes were strong for the week. The S&P 500 traded higher +1.7%, and the Nasdaq index was higher +3.5%.

Equities and yields are rebounding on gradually improving optimism on U.S. debt-limit negotiations.

Can higher interest rates halt the vibrant tech rally? Interest rates are rising again, and the tech sector is betting that the rate hiking cycle will soon be over.

The tech sector is susceptible to interest rates because it is capital-intensive. Tech companies need to borrow money to invest in research and development and acquire other companies. Higher interest rates make it more expensive for tech companies to do these things, which could slow their growth.

The global economy is growing, and people worldwide are using more technology. This is helping to offset the impact of higher interest rates on the tech sector. However, the tech sector also benefits from strong global demand for its products and services.

As a result, the tech sector is betting that the rate-hiking cycle will soon be over. If this happens, it could lead to a further rally in tech stocks.

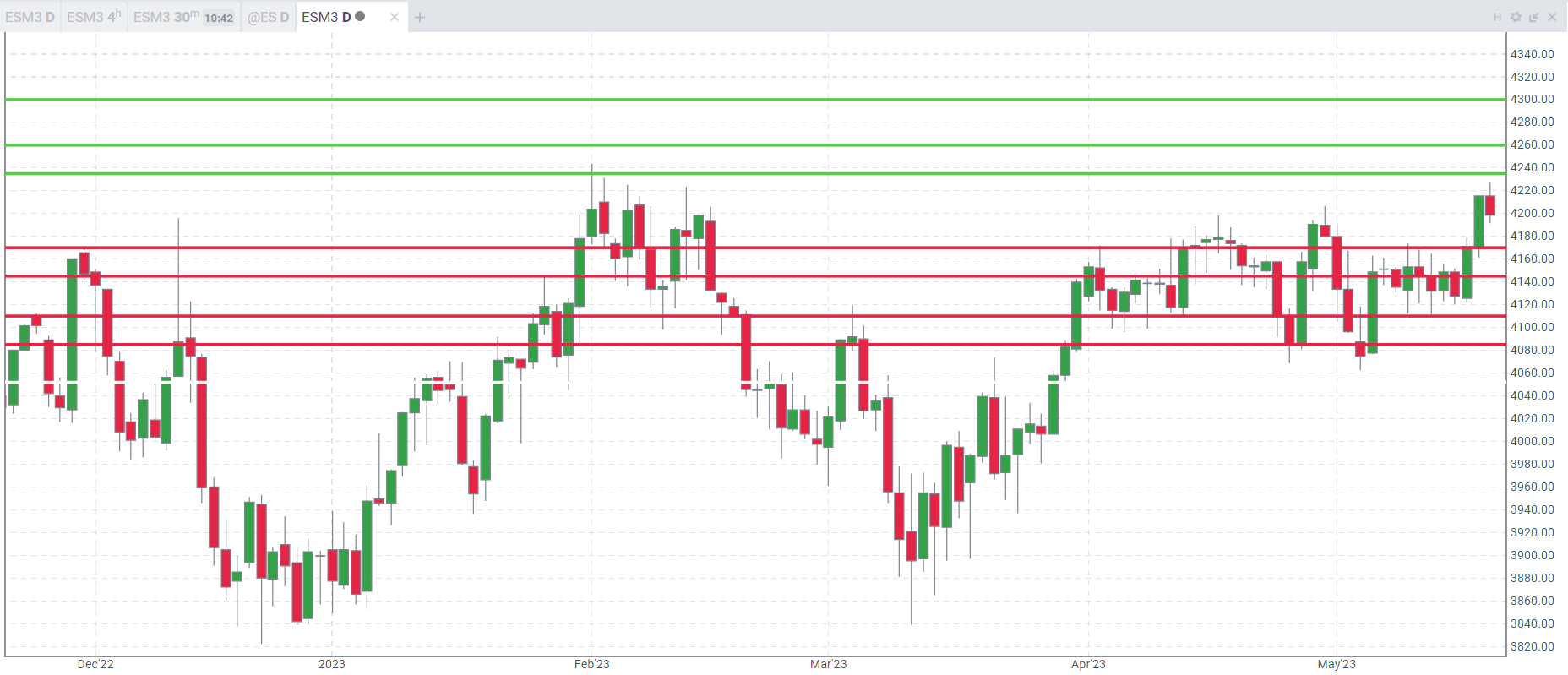

A few key short-term levels for the S&P 500:

Upside: 4235,4260,4300

Downside: 4170,4145,4110,4085

U.S. Treasury futures prices tanked, and interest yields soared last week.

Even as Federal Reserve officials started questioning the pace of higher interest rates, James Bullard, the president, and CEO of the Federal Reserve Bank of St. Louis, said that higher interest rates are insurance against inflation and favored a rate hike in June.

Dallas Fed President Lorie Logan said that a pause in rate hikes is not in order as of right now, though that could change in the coming weeks depending on incoming data. She said, “After raising the target range for the federal funds rate at each of the last 10 FOMC meetings, we have made some progress. The data in the coming weeks could yet show that it is appropriate to skip a meeting. As of today, though, we aren’t there yet.”

The chances of a Fed Funds (June 14) rate remaining on hold are still high at 82%, with a 17% chance of a 25 basis point hike. Traders have been removing and adjusting the possibility of future interest rate cuts in December 2023 to June 2024 meetings.

U.S. Treasury yields compared to the last week:

30-Year yield 3.93% VS. 3.79%

10-Year yield 3.67% VS. 3.47%

5-Year yield 3.73% VS. 3.45%

2-Year yield 4.27% VS. 3.99%

2-10 Yield spread -0,59% VS. -0.52

Gold was seen as the “ultimate” debt ceiling risk hedge. This has proven to be the total opposite. We are well below the 50-day and at must-hold levels. A close slightly lower and the 100-day moving average come into play.

Another go-to for “tail risk” traders is deep OTM S&P 500 put hedges, which also are a losing position at this stage as stock indexes have been higher.

The debt limit deadline is quickly approaching. Many analysts say it could happen between June 1-9. As a result, we expect the market volatility to increase if no agreement is inked in the coming ten days.

The grain markets skidded on the news last week that the Ukraine Black Sea grain deal has been extended for two more months. That means there is potential for more supply on the market.

Last week, corn and soybean futures for July expiration traded -4.8% and -5.9%.

The recent U.S. dollar index futures strength, improving U.S. weather, and weak global demand have also cast a negative tone on global grain prices.

According to the most recent COT report, hedge funds are net “short” agriculture futures for the first time since August 2020.

Do we fade the recent move? We are coming into an excellent seasonal time for prices in corn futures starting this Monday. Corn prices tend to peak in early June and bottom in early October.

The weather will be a key factor in the agricultural markets in the early season emergence in the Midwest. The weather has been ideal for planting so far. Here are some additional details about the best weather conditions for corn emergence:

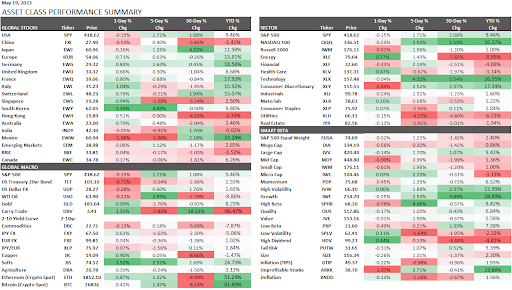

This performance chart tracks the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.

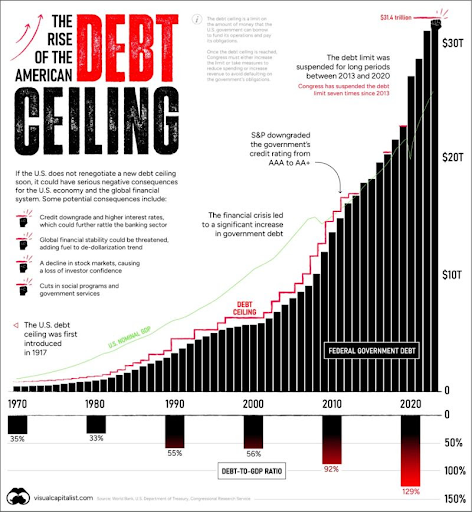

How did we get into this high debt situation? There are many factors: