Home › Market News › The Bitcoin Halving, Gold Prices, and Low Commodity Inventory Levels

The Economic Calendar:

MONDAY: Empire State Manufacturing Index (7:30a CT), Retail Sales (7:30a CT), Business Inventories (9:00a CT), NAHB Housing Market Index (9:00a CT), Retail Inventories (9:00a CT), NOPA Crush Report (11:00a CT), Mary Daly Speaks (7:00p CT)

TUESDAY: Building Permits (7:30a CT), Housing Starts (7:30a CT), Redbook (7:55a CST), Industrial Production/Capacity Utilization (8:15a CT), Manufacturing Production (8:15a CT), 52-Week Bill Auction (10:30a CT)

WEDNESDAY: MBA Mortgage Applications (6:00a CST), EIA Petroleum Status Report (9:30a CT), 20-Year Bond Auction (12:00p CT), Beige Book (1:00p CT), Loretta Mester Speaks (4:30a CT)

THURSDAY: Jobless Claims (7:30a CT), Philly Fed Manufacturing Index (7:30a CT), John Williams Speaks (8:15a CT), Existing Home Sales (9:00a CT), EIA Natural Gas Report (9:30a CT), Raphael Bostic Speaks (10:00a CT)

FRIDAY: Austan Goolsbee Speaks (9:30a CT), Baker Hughes Rig Count (12:00p CT)

Key Events:

The geopolitical situation between Israel and Iran will take center stage this week. How will Israel respond to the attack by Iran?

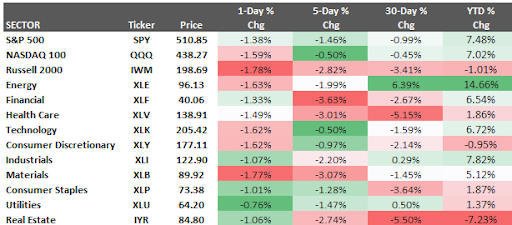

Last week, the S&P 500 fell by -1.46%, and the Nasdaq fell by -0.50%.

The retreat in stocks last week was primarily due to yet another hotter-than-anticipated consumer price index (CPI) report published on Wednesday. Traders reacted to the CPI data by paring back their Fed rate cut expectations.

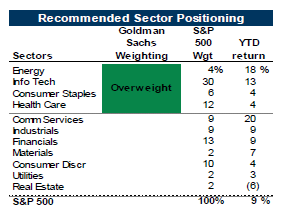

All stock sectors we tracked were down during the week, with the most significant losses coming from the financial, healthcare, and materials sectors. Below are Goldman Sachs sector recommendations.

Source: Goldman Sachs

The first quarter (Q1) earnings reporting season for US companies begins this week. This is a time when investors closely watch the financial results of publicly traded companies, which can impact the overall stock market.

Here’s what traders will likely be paying attention to:

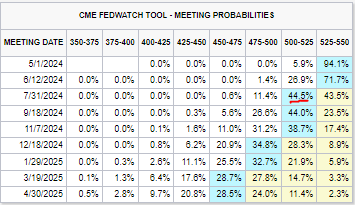

Traders reacted to the CPI data by paring back their Fed rate cut expectations and shutting the door on a 25 basis point cut in June. The market probabilities of a Fed rate cut have been pushed out into September.

Interest Rate Cuts on Hold for June:

CME Fedwatch

Is the halving priced into the market already? We think NO.

We thought Bitcoin would likely stay around $70k per BTC around the halving; however, the geopolitical situation over the weekend tanked BTC to around $64k.

Bitcoin is days away from its fourth halving. So, as is customary every four years, now is the time to speculate. If Bitcoin were to follow a similar post-halving growth trajectory than in the previous cycles, we would expect BTC to go anywhere between $140k and $4.5m per coin.

Miners’ reliance on transaction fees will grow. BTC miner revenue consists of the block reward, which will drop 50% from 6.25 to 3.125 BTC, and transaction fees paid by users.

Historically, a minority of miner revenue has been derived from fees. For example, over the last seven years, the proportion of miner revenue derived from fees has averaged ~5%. The halving will thus decrease the relative size of block reward-derived revenue in favor of fee-based revenue.

Early indications are for Gold futures to open higher on the geopolitical situation over the weekend.

Gold prices surged to record highs of $2,447 per ounce on Friday before pulling back slightly later to $2360.

This rally is driven by ongoing geopolitical tensions, overall financial uncertainty, and the expectation of interest rate cuts from the Federal Reserve. Traders seek safe-haven assets like gold due to worries about the stock market reaching record highs and inflation remaining stubbornly high.

However, despite the momentum pushing gold prices higher, some experts believe this upward trend may not be sustainable throughout 2024.

A strengthening US dollar and the possibility of positive real interest rates (meaning interest rates that outpace inflation) could dampen gold’s appeal. Additionally, central banks may be less active in buying gold, further influencing prices. While the near future looks bullish for gold, some analysts predict prices to moderate later in 2024 and into 2025.

Commodities Index is up +7.6%, Gold is higher +14.5%, and Oil is up +22% YTD.

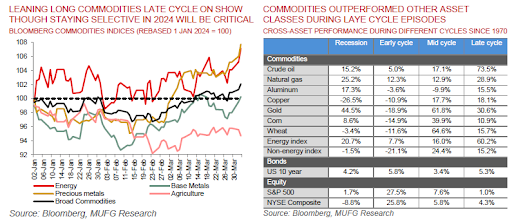

We are at the end of an economic cycle and months away from some form of “landing.” The economy seems to be nearing the end of its growth cycle, but a slowdown (landing) is likely still months away. This stage often triggers certain market behaviors in the commodity markets:

Historically, commodities have been a good investment during this late-cycle phase. This is because demand stays high while stockpiles of these raw materials dwindle.

Evidence supports this:

We believe the shortage of commodities is a bigger risk than a sudden global recession. As a result, we expect the price difference between nearby and future contracts (backwardation) to become even more pronounced. Overall, we are leaning long commodities in the next year.

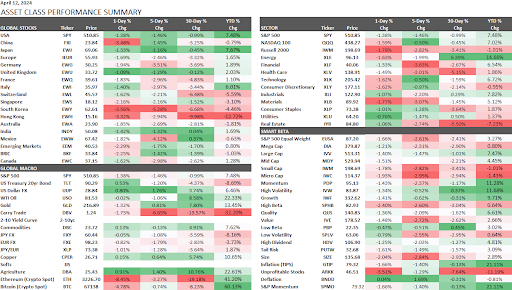

These performance charts track the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.