Home › Market News › Q1 Market Performance

The Economic Calendar:

MONDAY: PMI Manufacturing, ISM Manufacturing Index, Construction Spending, 3-Month Bill Auction, 6-Month Bill Auction, Investor Movement Index

TUESDAY: Motor Vehicle Sales, Factory Orders, JOLTS, Loretta Mester Speaks

WEDNESDAY: MBA Mortgage Applications, ADP Employment Report, International Trade in Goods and Services, PMI Composite Final, ISM Services Index, EIA Petroleum Status Report, 4-Month Bill Auction

THURSDAY: Challenger Job-Cut Report, Jobless Claims, James Bullard Speaks, EIA Natural Gas Report, 4-Week Bill Auction, 8-Week Bill Auction, Baker Hughes Rig Count, Fed Balance Sheet

FRIDAY: Employment Situation, Consumer Credit

Futures Expiration and Rolls This Week:

MONDAY: Gold futures have rolled from April (J) to June (M)

Key Events:

A good week on Wall Street ended with stock indexes higher. The S&P 500 gained 3.4% for the week, and the Nasdaq index climbed 3.2%.

Last week, there was a good trading room discussion on the” tale of two markets.” Nasdaq (QQQ) vs. Russell 2000 (IWM) was discussed, and the Q1 return dispersion was large, QQQ +20.5% and IWM +2.3%.

Of course, the Nasdaq is large-cap and tech-heavy, and the Russel 2000 is a small-cap U.S. stock market index that makes up the smallest 2,000 stocks in the Russell 3000 Index.

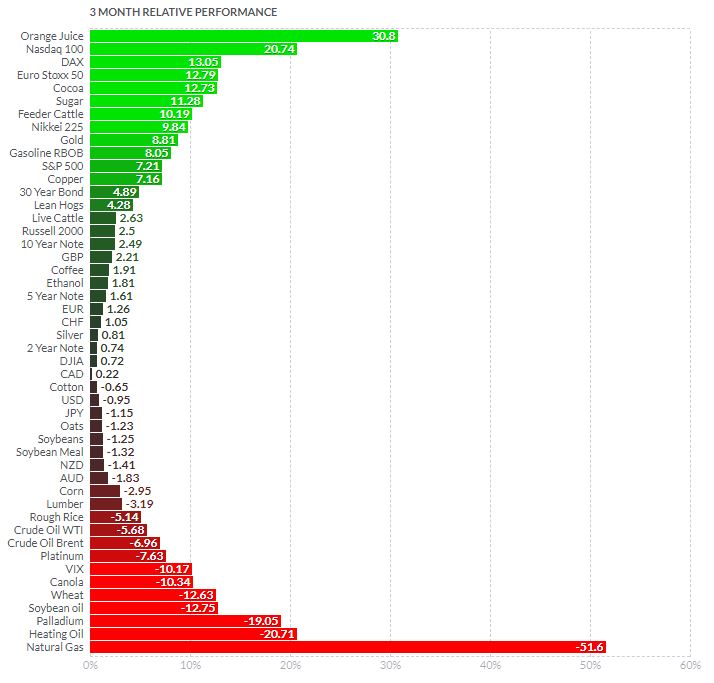

The Q1 Good, Bad, and Ugly:

Winners were Bitcoin +73%, Unprofitable Stocks (ARKK) +29%, Nasdaq +20% 35%, and Consumer Cyclical +15.7%

Losers were Natural Gas -52%, U.S. Regional Banks -24%, Oil -8%, Biotech -6%, and Energy -5%

A few key short-term levels for the S&P 500:

Upside: 4160,4210,4220

Downside: 4083, 4060,4025

Blackrock says The Federal Reserve will keep raising interest rates despite traders betting otherwise as fears of a banking crisis convulse markets. They believe the markets are wrong in expecting imminent U.S. rate cuts as the economy lurches toward a recession.

Blackrock strategists do not see rate cuts this year – they see a new, more nuanced phase of curbing inflation ahead: less fighting but still no rate cuts.

THE FED ISN’T DONE YET – Powell has delivered exactly what he said he would throughout this tightening cycle. He told us that the Fed is not cutting this year. Fed Chair Powell and their peers have clarified that banking sector troubles won’t halt their battle against inflation.

The view is the opposite of T.D. Securities and DoubleLine Capital L.P., who say the Fed is mistaken about the need to keep raising interest rates as the risk of recession grows.

U.S. Treasury yields current yield compared to the last newsletter:

30-Year yield 3.65%vs. 3.65%

10-Year yield 3.47% vs. 3.38%

5-Year yield 3.58% vs. 3.441%

2-Year yield 4.029 vs. 3.775%

2-10 Yield spread -0.55% vs. -0.39%

OPEC+ met to discuss oil production over the weekend. The expectation from February was for the committee to cut overall output by 2 million barrels per day and to hold that line.

OPEC+ oil producers on Sunday announced further oil output cuts of around 1.16 million barrels per day, which traders said would cause an immediate rise in prices.

According to Reuters, this brings the total volume of cuts by OPEC+ to 3.66 million barrels per day.

Will recession again be delayed by stimulus? The “pain trade” thought process goes this way – if the labor market doesn’t crack, inflation stays high, and the market reprices lower.

Positioning ahead of Q2 has the Fed cutting 160bps after May. Position interest is long big tech, a recession is a slam-dunk, short small caps & banks, and long gold as the U.S. dollar in a bear market. Could this reverse?

Valuations for stocks overall are also high historically, with the S&P 500 trading at about 18 times forward earnings estimates compared to its long-term average P/E of 15.6x, according to Refinitiv Datastream. Note below the stretched P/E ratio of NVDA at 159x and the Software Applications industry.

In a report earlier this week, Morgan Stanley strategists said earnings estimates were 15-20% too high even “before the recent banking events.”

Strategists say that “bank deposits are in the midst of a two-stage shift” – the first phase of the bank run, deposits were pulled from banks driven by “solvency concerns.”

But as solvency fears fade, a second stage is emerging, driven by interest rate differentials primarily between regional banks that cannot match the Fed Funds rate.

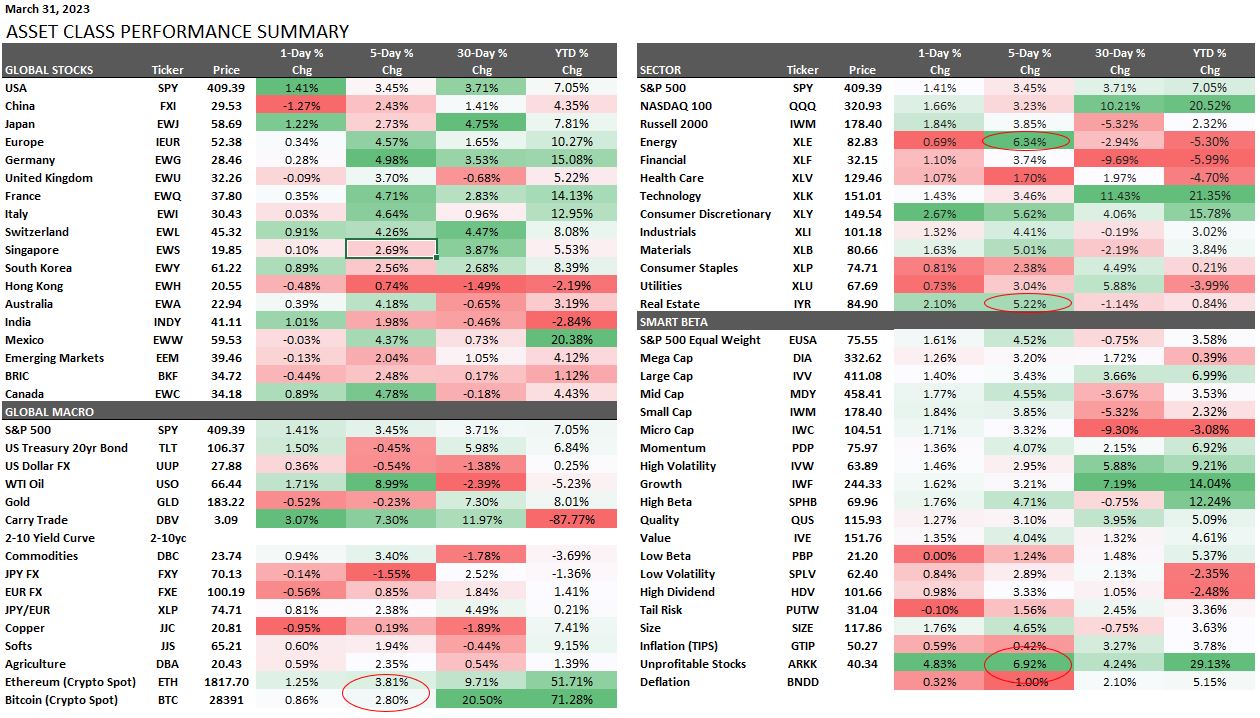

This performance chart tracks the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.

I’m not a big Taylor Swift music fan, but I walked past this quote at Northwestern University, and it rings so true as a trader trying to expand their strategy playbook. DON’T BE AFRAID TO FAIL!!!