Home › Market News › Position Sizing, Yield Curve Projections, and the January Jobs Report

The Economic Calendar:

MONDAY: 3-Month Bill Auction, 6-Month Bill Auction, Investor Movement Index

TUESDAY: International Trade in Goods and Services, 3-Yr Note Auction, Consumer Credit

WEDNESDAY: MBA Mortgage Applications, John Williams Speaks, Wholesale Inventories, EIA Petroleum Status Report, 4-Month Bill Auction, 10-Yr Note Auction

THURSDAY: Jobless Claims, EIA Natural Gas Report, 4-Week Bill Auction, 8-Week Bill Auction, 30-Yr Bond Auction, Fed Balance Sheet

FRIDAY: Consumer Sentiment, Baker Hughes Rig Count, Treasury Statement, Patrick Harker Speaks

Futures Expiration and Rolls This Week:

There are no expiration or rolls this week

Key Events:

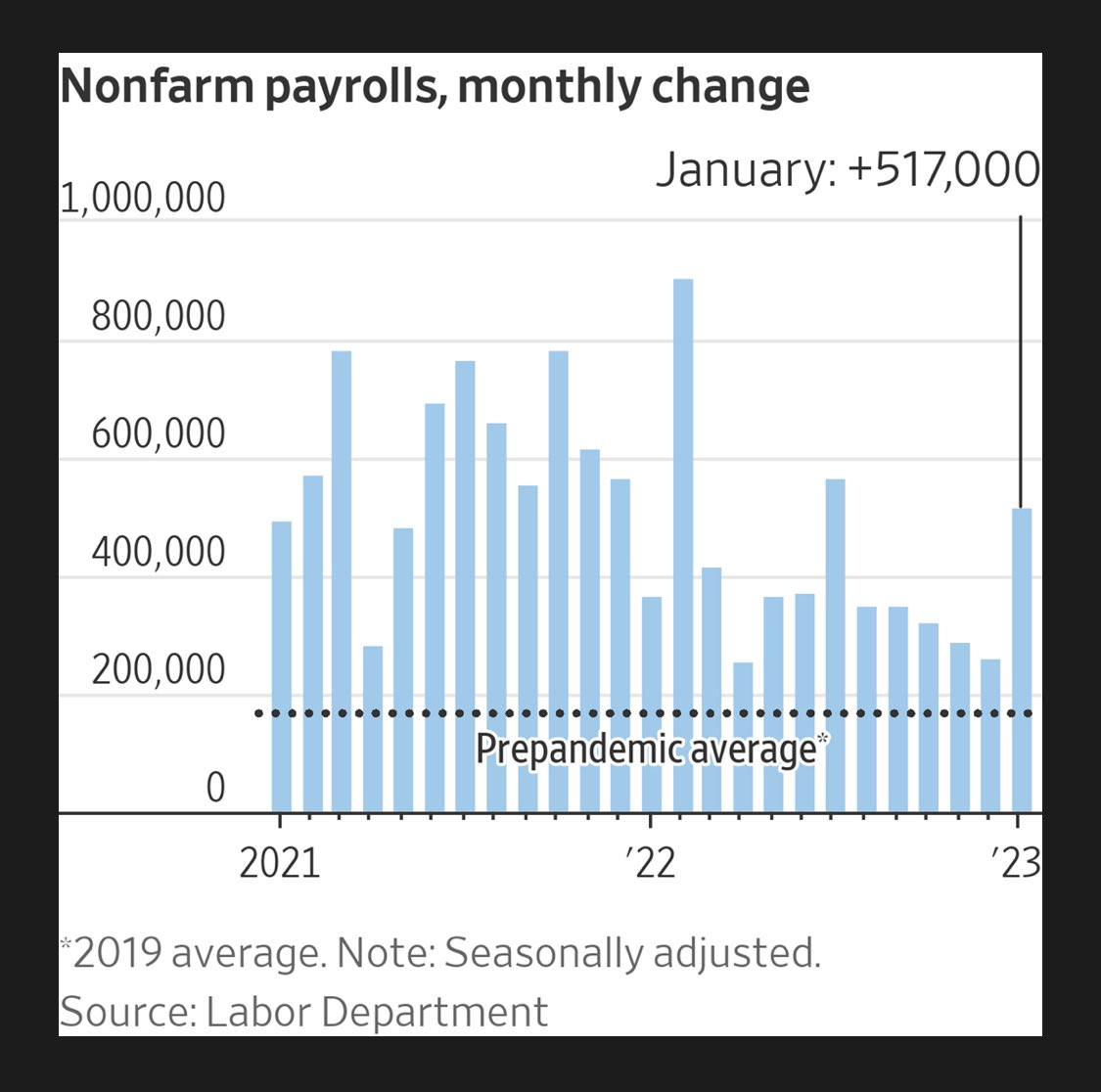

Weak outlooks for tech heavyweights such as Amazon and Microsoft and a blowout employment number heightened expectations for Fed hawkishness and injected a fresh note of uncertainty.

An index of nonprofitable technology companies compiled by Goldman Sachs is up 28% after sinking in 2022. Likewise, the bank’s index of the most-shorted stocks in the Russell 3000 Index has climbed 23% following its worst year.

We expect S&P 500 to struggle with the S&P 4210 resistance level and hope we are in a new balance area between the 4100-4210 range. Shorts could come back in under 4100.

In January, the U.S. Non-Farm Payrolls figure was 517k, significantly exceeding the most optimistic economist expectation. This strong hiring was spread between leisure and hospitality, professional and business services, and healthcare sectors.

The robustness of the employment report has some thinking inflation could return in the near future.

Not so fast. Now that jobs data has surprised to the upside, markets are coming around to Powell’s entire post-FOMC comments instead of taking his comment on disinflation out of context.

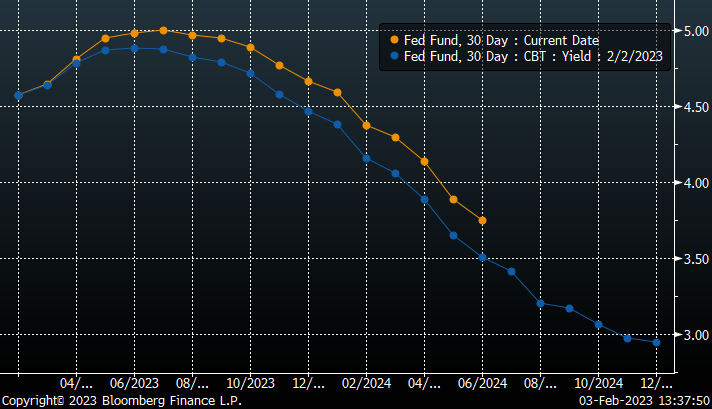

The market’s extraordinary resurgence and movement in January indicate that traders do not believe the Federal Reserve will keep interest rates high for long.

This skepticism is despite the central bank’s projection that they are unlikely to cut rates this year.

Johan Grahn, head of exchange-traded funds at Allianz Investment Management, noted, “The markets are calling their bluff” about the Fed’s outlook. In the press conference, Fed Chairman Jerome Powell attributed the divergence to a “difference in perspective…on how fast inflation will come down.”

The peak rate is back to 5% in the below graphic.

U.S. Treasury yields current yield compared to the last newsletter:

30-Year yield 3.616% vs. 3.62%

10-Year yield 3.526% vs. 3.505%

5-Year yield 3.66% vs. 3.61%

2-Year yield 4.291% vs. 4.20%

2-10 Yield spread -0.769% vs. -0.69%

Last week, the tech giants Facebook (Meta), Apple, Alphabet (Google), and Amazon released their quarterly earnings reports.

Meta, the parent company of Facebook, reported higher-than-expected revenue in its fourth-quarter earnings, leading to a surge in its stock price.

On the other hand, Apple’s revenue decreased year-on-year for the first time since 2019, while Alphabet and Amazon’s earnings were lower than expectations, respectively.

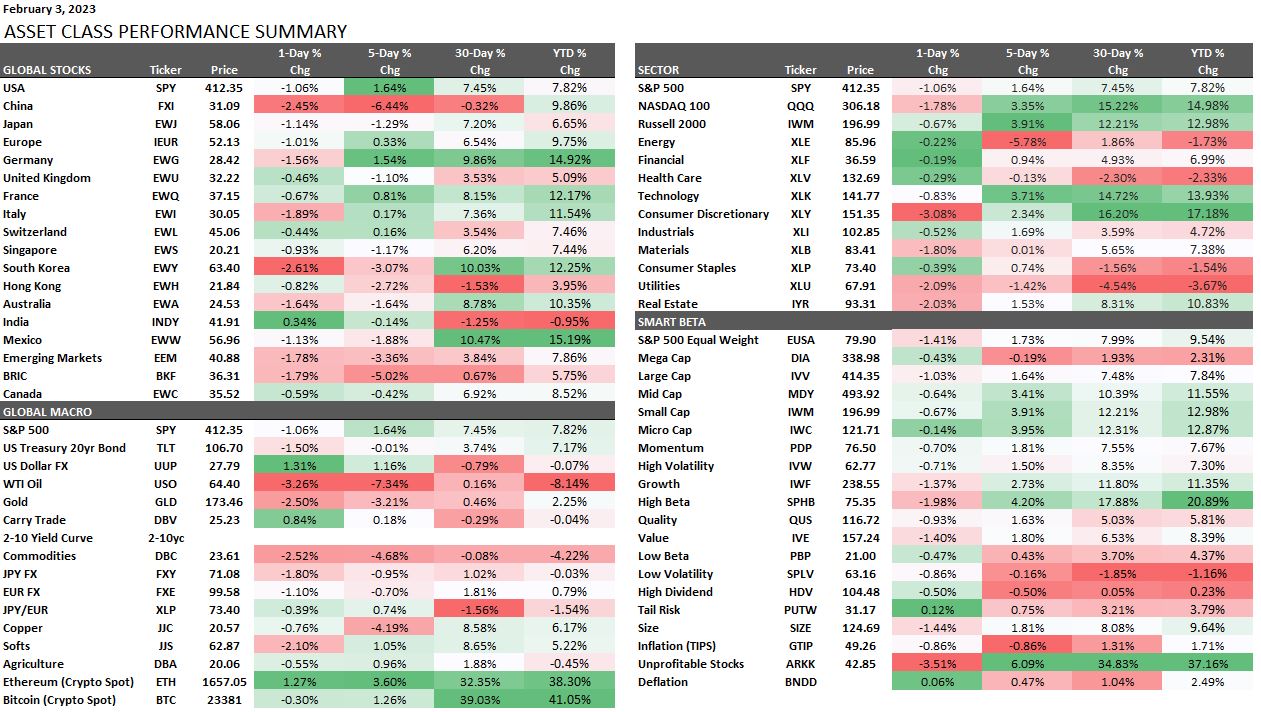

As you can see from the graphic below, value stocks and the healthcare, energy, and consumer staples sectors have struggled year-to-date. Conversely, technology, communication service, and consumer cyclical have outperformed.

The European Central Bank (ECB) took action as predicted, increasing the deposit rate by 50 basis points (bp) and reaffirming their desire to continue tightening by an additional 50 bps in March. ECB President Christine Lagarde explained that underlying inflationary pressures, fiscal measures, and wage growth were the reasons behind this decision.

At the press conference, Lagarde noted that the bank would not reach peak rates by the next meeting in March, indicating that the hopes for a pause in May may still need to be fulfilled. Furthermore, she emphasized keeping rates higher to ensure inflation subsides.

Economists forecast that ECB policymakers think there will be at least two more rate hikes of 25bps or 50bps in May, signaling a scaling back of the hawkish market pricing for 2023.

The zero days to expiration (0DTE) call buying frenzy generates some seriously volatile market behavior – as the three major dealers (Susquehanna, CItadel, and Goldman Sachs) scramble to hedge 0DTE buying in increasingly thinly traded markets.

It’s all about the lack of liquidity. On some days, these 0DTE (Zero Days to Expiration) options represent greater than 50% of the dollar trading flow in the stock or ETF.

Meme of the Week – Powell…Chair Powell!!