Home › Market News › Oil Stocks, Energy Futures & An Economic Dilemma

The Economic Calendar:

MONDAY: Neel Kashkari Speaks (6:00p CT)

TUESDAY: NFIB Business Optimism Index (5:00a CT), Redbook (7:55a CT), 3-Year Note Auction (12:00p CT)

WEDNESDAY: MBA Mortgage Applications (6:00a CT), Core Inflation Rate (7:30a CT), CPI (7:30a CT), Michelle Bowman Speaks (7:45a CT), Wholesale Inventories (9:00a CT), EIA Petroleum Status Report (9:30a CT), Austan Goolsbee Speaks (11:45a CT), 10-Year Note Auction (12:00p CT), FOMC Minutes (1:00p CT)

THURSDAY: Jobless Claims (7:30a CT), PPI (7:30a CT), John Williams Speaks (7:45a CT), EIA Natural Gas Report (9:30a CT), Susan Collins Speaks (11:00a CT), WASDE Report (11:00a CT), 30-Year Bond Auction (12:00p CT), Raphael Bostic Speaks (12:30a CT)

FRIDAY: Import & Export Prices (7:30a CT), University of Michigan Consumer Sentiment (9:00a CT), Baker Hughes Rig Count (12:00p CT), Raphael Bostic Speaks (1:30p CT), Mary Daly Speaks (2:30p CT)

Key Events:

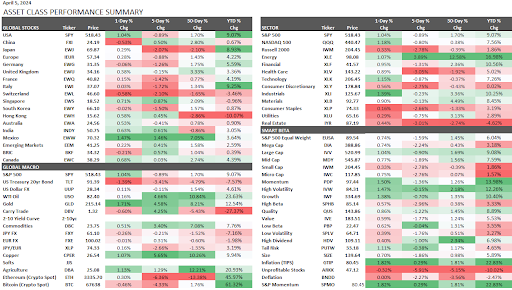

Stocks rebounded Friday after encouraging jobs data, erasing much of the Thursday selloff. The S&P 500 and Nasdaq 100 were still down for the week,-0.89% and 0.80%.

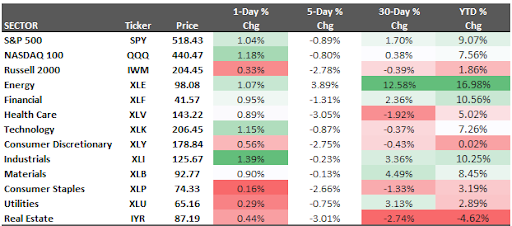

The Energy sector was the best performer of the week, +3.89%. Healthcare, Consumer Discretionary, and Real Estate sectors lagged -3.05%, -2.75%, and -3.01%.

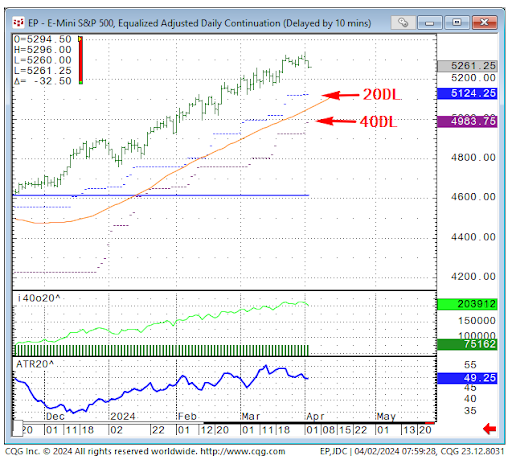

This trade is not easy! Markets don’t go in a straight line forever, and a clear breach of the trendline in the S&P 500 would be our first clue that the upward trend may be drawing to a close.

That said, trends can often continue for much longer than most people think, so we rely heavily on our models.

We consult with Totem Asset Group’s benchmark academic project for further guidance as a reasonably good trend following proxy. In this “fast’ model, a breach of the 20-day low in the S&P 500 would cause long liquidation, and a breach of the 40-day low would cause a short initiation. “Slower” models could be a little more forgiving, but in either case, trail those protective “sell stop” orders and enjoy the ride!

Source: Totem Asset Group

Fed Chair Jerome Powell said recently that interest-rate cuts are still likely this year despite a strong economy. In particular, he said stronger-than-expected inflation data for January and February hadn’t shaken the Fed’s policy outlook. However, President of the Federal Reserve Bank of Minneapolis Neel Kashkari said if inflation continued to move sideways, “that would make me question whether we needed to do those rate cuts at all.”

This suggests inflation data will be scrutinized intensely, particularly given a recent rise in crude oil prices.

Has the Fed recently shifted its focus from fighting inflation to supporting a healthy job market?

The Federal Reserve needs help to balance two goals: keeping unemployment low and prices (inflation) stable. These goals usually work together, but sometimes one takes priority.

Our Takeaways:

The Federal Reserve has a dual mandate: maximum employment and price stability.

Financial markets are set for a busy week with key data releases and events that will influence investor decisions.

Traders will eagerly await the release of the minutes from the Federal Reserve’s March policy meeting. This comes after recent strong labor market data dampened expectations of an interest rate cut in the near future.

Market participants hope to glean further insights into the Fed’s future monetary policy direction by scrutinizing the minutes and the upcoming consumer inflation report.

The financial markets seem to send a mixed message about the U.S. government’s growing budget deficits. Despite widespread concern about the high and persistent deficits, the prices of U.S. Treasury securities haven’t reflected this worry. Here’s why it’s confusing:

In short, the market’s pricing of U.S. Treasuries doesn’t seem to reflect the anxieties surrounding the U.S. budget situation fully.

U.S. large-cap Energy is the surprise winner YTD but is still oversold on a longer-term (100-day) basis.

Some traders use the Energy sector as a unique hedge against a geopolitically driven oil price shock.

Oil is surging to another yearly high as demand expectations rise, supply falls, geopolitical risks rise, and OPEC March Oil output falls.

The upcoming Bitcoin halving in mid-April is generating significant buzz. This time, with a larger audience, it could drive additional demand for Bitcoin. However, there are countervailing factors:

Every trader has a story, and you’ll learn more from their failures than wins.

Instead of asking a successful trader, how did you make all that money?

Ask: “When did you almost lose it all? What did you learn?”

These performance charts track the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.