Home › Market News › Crypto Volatility, Wheat Futures, and the BOJ Yield Curve

The Economic Calendar:

MONDAY: Chicago PMI, Dallas Fed Manufacturing Survey, 3-Month Bill Auction, 6-Month Bill Auction

TUESDAY: PMI Manufacturing Final, ISM Manufacturing Index, Construction Spending, JOLTS

WEDNESDAY: Motor Vehicle Sales, MBA Mortgage Applications, ADP Employment Report, Treasury Refunding Announcement, EIA Petroleum Status Report, 4-Month Bill Auction

THURSDAY: Challenger Job-Cut Report, Jobless Claims, Productivity and Costs, PMI Composite Final, Factory Orders, ISM Services Index, EIA Natural Gas Report, 4-Week Bill Auction, 8-Week Bill Auction, Fed Balance Sheet

FRIDAY: Employment Situation, Baker Hughes Rig Count

Key Events:

The July jobs report is expected to show a slight moderation from the recent trend, with nonfarm payroll employment forecast at 200K. This would be down from the 209K job additions in June but still point to a tight labor market.

The Federal Reserve will closely watch the report, as it will provide further evidence on the state of the economy. If the report shows that the labor market is still strong, it could pressure the Fed to raise interest rates more aggressively to cool inflation.

However, if the report shows that the labor market is starting to soften, it could give the Fed some breathing room to pause its rate hiking cycle.

Ultimately, the July jobs report will be just one piece of data that the Fed will consider when making its monetary policy decisions. However, it will likely be a significant factor in the debate over whether the Fed is too loose or tight.

Source: Trading Economics

The Federal Reserve announced last Wednesday it had raised its key interest rate by 0.25% to a target rate between 5.25% – 5.5%, the highest level in 22 years.

Although nominal short-term interest rates have reached their highest levels since 2001, real (inflation-adjusted) rates remain moderate. Real interest rates are important for both currencies and risk assets and likely to be an important driver over time.

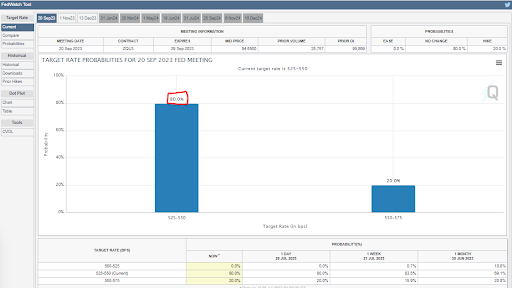

The Fed has time to access two additional inflation and jobs data reports before the next Fed meeting on September 20.

The market is pricing an 80% probability of no change in fed fund rates and 20% of a 25 basis point hike at the September meeting.

CURRENT U.S. TREASURY YIELDS:

30-Year yield 4.01%

10-Year yield 3.95%

5-Year yield 4.17%

2-Year yield 4.88%

2-10 Yield spread -0.92%

Source: CME Group Fedwatch

The crude oil markets are grappling with the imminent prospect of a supply shortage. Despite the backdrop of macroeconomic conditions, there appears to be a tug-of-war between market fundamentals and prevailing sentiments among oil traders. Notably, the remarkable surge in global oil demand, which reached an unprecedented 2 million barrels per day, has been largely overlooked.

According to the International Energy Agency, the current trajectory indicates that global oil demand is set to hit a historically tight level of 101.9 million barrels per day. Exxon Mobil has already observed record demand this year, and they anticipate another record-breaking demand for the following year.

However, it is important to acknowledge that genuine concerns about potential risks to the global economy have arisen. The market is evaluating the implications of interest rates rising to levels many traders have never encountered.

At the recent BOJ rate decision, the Bank of Japan (BOJ) surprised financial markets by loosening yield curve control.

They made no changes to their interest rates. Still, they voted to conduct “yield curve control” policies with greater flexibility, allowing the 10-yr JGB yield to rise to 1.0% while maintaining the target at 0.50%.

The news briefly boosted the yen before the currency returned to little change against the dollar.

Many traders’ positions were stopped out of the widespread carry trade – long EURJPY. In the past, EURJPY has been an excellent barometer for carry-trade and risk-taking (Risk-On) behavior.

Last week’s news that Russia destroyed Ukrainian grain facilities along the Danube sent corn and wheat futures soaring higher.

September wheat futures traded limit-up last Monday, closing 60 cents higher at 757-4. The high for the week came on Tuesday, while the contract had expanded limits, trading up to 777-2, before settling lower on Wednesday, Thursday, and Friday.

After the volatile week, September wheat futures closed just 6-6 cents higher at 704-2. This week traders are looking at upside resistance between 744-745 and support in the 685 area.

U.S. Q2 GDP (growth) is much stronger than expected despite recession calls and aggressive interest rate rises.

The headline reading showed the economy grew by 2.4% vs economist expectations of 1.8%.

In light of the recent decline in inflation rates within the United States and the unexpected resilience of the economy, market sentiment is increasingly inclined towards the belief that the Federal Reserve might successfully attain a coveted “soft landing.”

This rare and elusive achievement involves effectively reining inflationary pressures without substantially harming the broader economy.

Bitcoin Volatility Hits Historic Low

Bitcoin’s historical 30-day volatility has reached its lowest point since the start of 2020. This suggests that the market is becoming increasingly range-bound, with prices trading between $25,000 and $31,800 since March.

Regarding low volatility, FRNT CEO Stephane Ouellette told CoinDesk that “this type of environment historically has not persisted for long.” He pointed out that FRNT’s data analysis suggests that “some of the most significant volatility spikes have emerged out of such environments.”

Ouellette also noted that “historically, in albeit relatively short history of BTC, resolves more often than not in a directional move to the upside.” This suggests the current low volatility could be a precursor to a larger move in Bitcoin’s price.

Trading Activity Subdued in 2023

Along with the historically low volatility, 2023 has also been characterized by depressed trading activity. For instance, in 2023, the average daily BTC/USD volume on Bitfinex is $44.83 million. 2022 this metric stood at $148.37 million; in 2021, it was $397.84 million.

This subdued trading activity is likely due to several factors, including the overall sell-off in the crypto market, the liquidation of many large positions, and the lack of institutional interest.

This performance chart tracks the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.

Our trade desk had risk over set limits last week. So, obey your risk RULES, or don’t have rules at all!

If you dislike the RULE, CHANGE them before the trade position is on, definitely not after the trade.