Home › Market News › All Eyes on the Fed and the January Jobs Report

The Economic Calendar:

MONDAY: Dallas Fed Manufacturing Survey, 3-Month Bill Auction, 6-Month Bill Auction

TUESDAY: FOMC Meeting Begins, Employment Cost Index, Case-Shiller Home Price Index, FHFA House Price Index, Chicago PMI, Consumer Confidence, Farm Prices

WEDNESDAY: MBA Mortgage Applications, ADP Employment Report, Treasury Refunding Announcement, PMI Manufacturing, ISM Manufacturing Index, Construction Spending, JOLTS, EIA Petroleum Status Report, 4-Month Bill Auction, FOMC Announcement, Fed Chair Press Conference

THURSDAY: Motor Vehicle Sales, Challenger Job-Cut Report, Jobless Claims, Productivity and Costs, Factory Orders, EIA Natural Gas Report, 4-Week Bill Auction, 8-Week Bill Auction, Fed Balance Sheet

FRIDAY: Employment Situation, PMI Composite, ISM Services Index, Baker Hughes Rig Count

Futures Expiration and Rolls This Week:

TUESDAY: First Notice Day for February (G) Gold Futures

Key Events:

All eyes on the Fed announcement Wednesday.

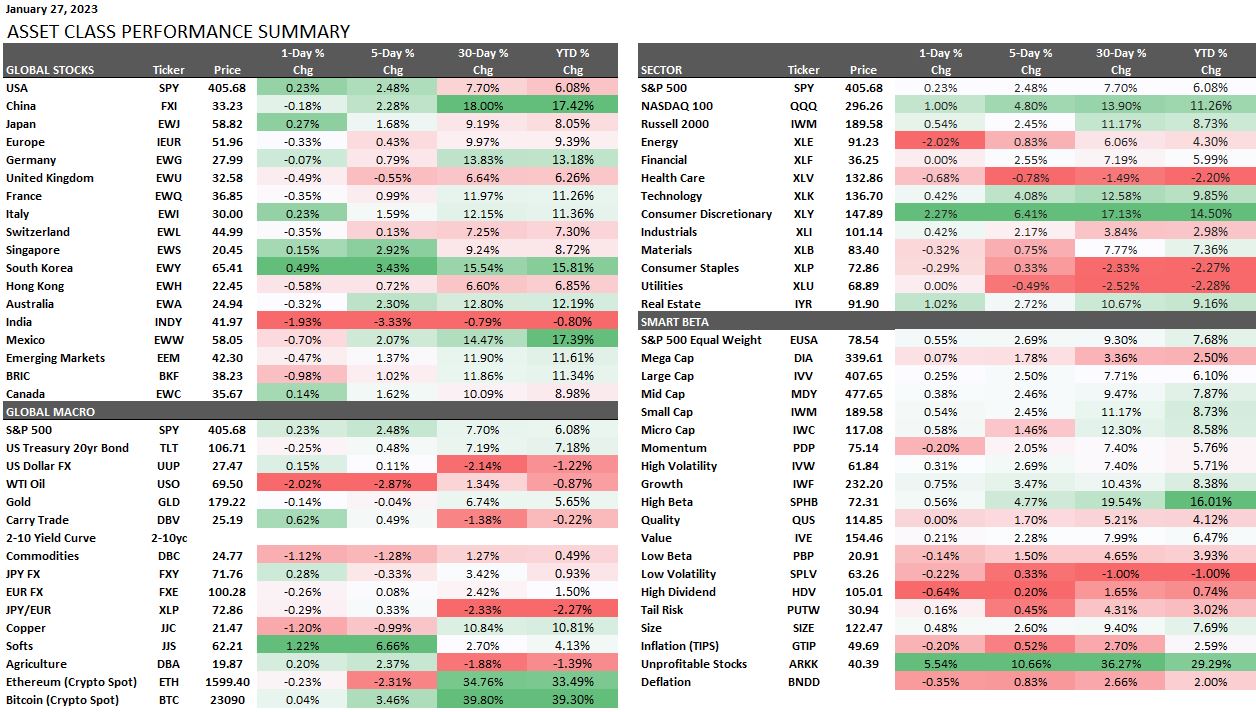

It was a winning week for stocks. The Nasdaq 100 climbed 4.8% to rack up a fourth straight week of gains, while the S&P 500 gained 2.48%.

The market has a case of FOMO at the beginning of the year as more speculative high beta stocks are up around 20% in the last 30 days. Case in point, shares of Tesla surged a whopping 33% on the week after reporting earnings (50% YTD), and popular growth stock ETF ARKK rallied 10% on the week.

Traders look for guidance from the Fed on Wednesday. The recent rally could be front-running the Fed. We could see the end of the recent rally if there is a 50 basis point hike or continued diligence in fighting inflation.

We expect S&P 500 to struggle with the 4050-4150 range and for Fed to try and push the index back below 4000.

Keep an eye on the grain markets.

A story gathering steam is a possible global food shortage. Concerns of food shortages are still real and have not gone away despite the recent pullback in grain prices. While we may see South American harvest pressure, real risks of another significant food price spike are growing.

As far as corn goes, we’re seeing significant ethanol demand. There are concerns that weather patterns in Brazil will turn dry ahead of the corn-growing season in Brazil. In the U.S., the USDA, in its last report, lowered the size of the U.S. 2022 corn crop more than expected, and the USDA lowered the U.S. 2022 soybean crop more than expected.

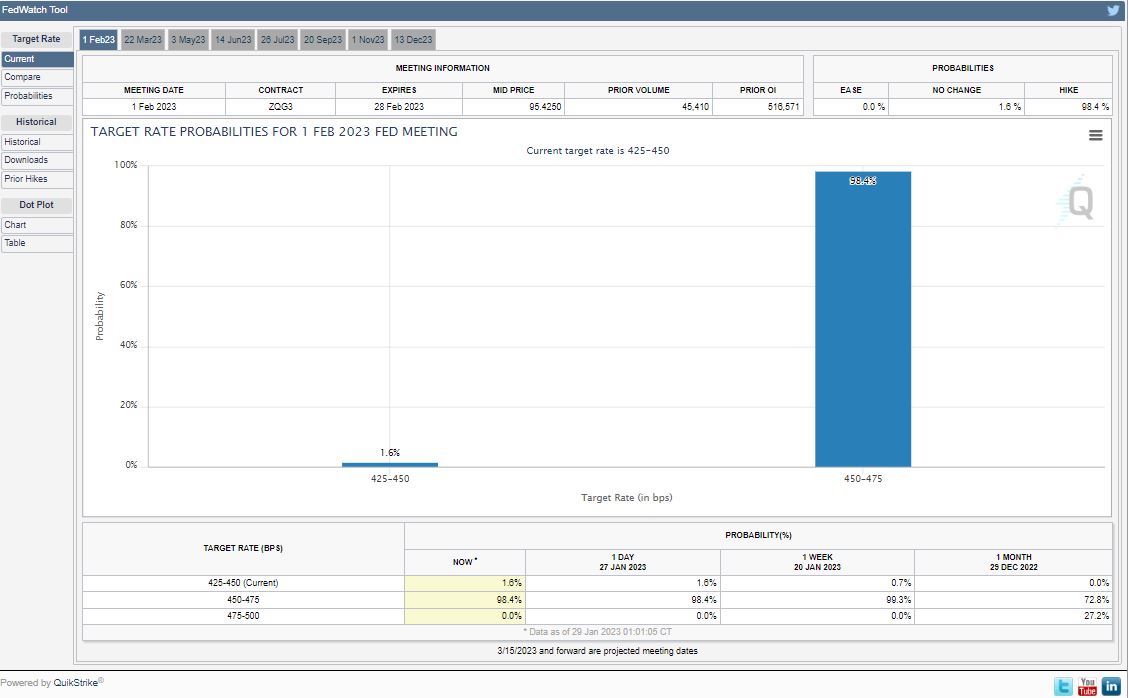

The Fed funds market has oscillated between anticipating another 25-50 basis point rate increase at the FOMC meeting this Wednesday. Based on Fed officials’ comments and media reports, traders have settled on a higher probability of a 25 basis point hike.

A 25 basis point hike will take the target federal funds rate to 4.50% to 4.75%. The consensus is that the Fed will continue its tightening policy and signal that more rate hikes are still in the mix.

We will buck the consensus and call for a 50 basis point hike. We see this as a credibility issue where the markets need to be aligned with the Fed’s forward-looking policy for 2023.

Recent economic data has been mixed. More robust than expected GDP growth at 2.9% (the consensus forecast was 2.6%); and a beat on weekly jobless claims (186,000 versus consensus of 205,000). The PCE price index, excluding food and energy (inflation report), rose 4.4% from a year earlier.

Traders no longer see inflation as an essential threat but are more worried about an economic slowdown or recession that brings lower prices.

U.S. Treasury yields current yield compared to the last newsletter:

30-Year yield 3.62% vs. 3.65%

10-Year yield 3.505% vs. 3.48%

5-Year yield 3.61% vs. 3.56%

2-Year yield 4.20% vs. 4.17%

2-10 Yield spread -0.69% vs. -0.69%

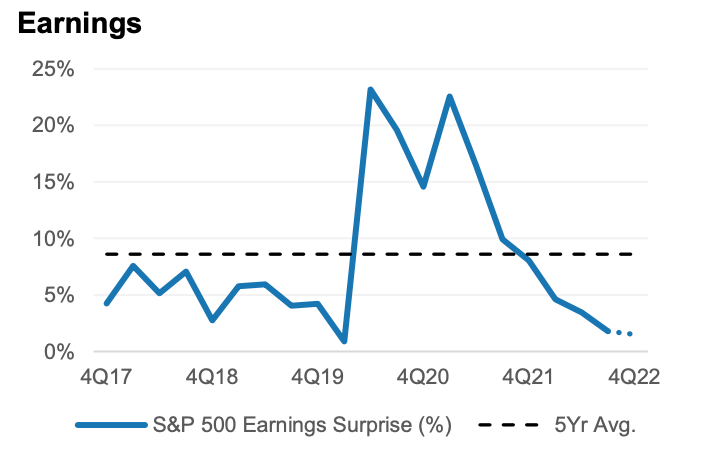

FOMO risk on rally chugs as earnings warnings mount. So far, the earnings season is well below average.

Solana token is having a nice run. The native token of the Solana Network has added $5.4 billion in market cap since reaching a 2yr low in December.

The bankruptcy of FTX dragged the SOL token lower. FTX was deeply involved in investing and developing the Solana ecosystem.

SOL reached an all-time high market cap of USD 78.28 billion in November 2021. The current market cap is $ 9.6 billion.

GitHub data suggests that Solana-related developer activity has remained relatively stable over the past year.