Home › Market News › Global Stocks, Euro Nat Gas, and a Crypto Rug Pull

The Economic Calendar:

MONDAY: Chicago Fed National Activity Index (7:30a CT), Dallas Fed Manufacturing Index (9:30a CT), 2-Year Note Auction (12:00p CT)

TUESDAY: Fed Logan Speech (3:20a CT), Redbook (7:55a CT), House Price Index (8:00a CT), S&P/Case-Shiller Home Prices (8:00a CT), CB Consumer Confidence (9:00a CT), Richmond Fed Manufacturing Index (9:00a CT), Dallas Fed Services Index (9:30a CT), Fed Barr Speech (10:45a CT), 5-Year Note Auction (12:00p CT), Fed Barkin Speech (12:00p CT), Money Supply (12:00p CT)

WEDNESDAY: MBA Mortgage Applications (6:00a CT), Building Permits (7:00a CT), Fed Barkin Speech (7:30a CT), New Home Sales (9:00a CT), EIA Petroleum Status Report (9:30a CT), 7-Year Note Auction (12:00p CT)

THURSDAY: Jobless Claims (7:30a CT), Durable Goods (7:30a CT), GDP (7:30a CT), Real Consumer Spending (7:30a CT), Fed Barr Speech (9:00a CT), Pending Home Sales (9:00a CT), EIA Natural Gas Report (9:30a CT), NY Fed Treasury Purchases (9:30a CT), Kansas Fed Composite Index (10:00a CT), Fed Bowman Speech (10:45a CT), Fed Hammack Speech (12:15p CT), Fed Harker Speech (2:15p CT), Fed Balance Sheet (3:30p CT)

FRIDAY: Personal Consumption Expenditures (7:30a CT), Retail/Wholesale Inventories (7:30a CT), Chicago PMI (8:45a CT), Baker Hughes Rig Count (12:00p CT)

Key Events:

The stock market generally reacts to tariff news with short-term volatility and sector-specific price shifts, often calming once clarity emerges. For March 1, 2025, tariffs on Canada and Mexico, expectations are mixed: pessimists anticipate a trade war sparking inflation and market drops, optimists hope for delays or mitigation, and many are simply watching for the next signal.

With only a week until the deadline, trader nervousness is palpable, but the outcome hinges on whether Trump follows through or blinks again.

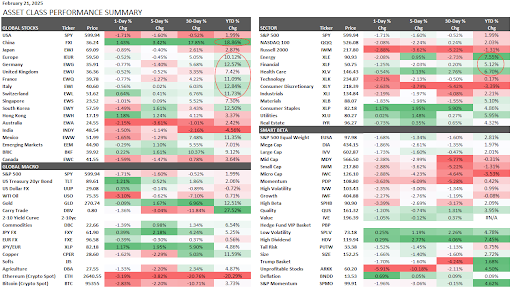

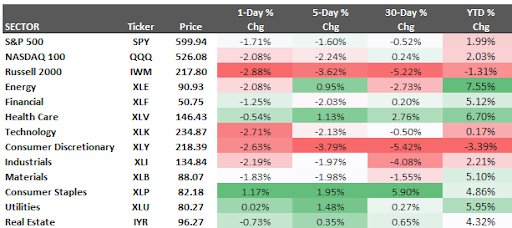

The market’s recent shift in sentiment has investors scrambling for the perceived safety of defensive stocks, raising concerns about a potential economic slowdown. A pronounced rotation away from cyclical sectors and into consumer staples has become increasingly evident since the recent change in administration.

Over the past month, consumer staples have outperformed, gaining 5.6%, while consumer discretionary stocks have faltered, declining 5.3%. This divergence suggests growing apprehension among traders about the economy’s near-term prospects.

The shift is further underscored by this week’s trading patterns, which have seen growth and momentum stocks take a significant hit while staples have attracted renewed interest.

This defensive positioning raises questions about the new administration’s economic agenda. A market driven by demand for canned goods and other staples hardly aligns with a narrative of robust growth. The current market dynamics suggest a focus on “making America stock up on non-perishables” rather than anticipated broader economic revitalization.

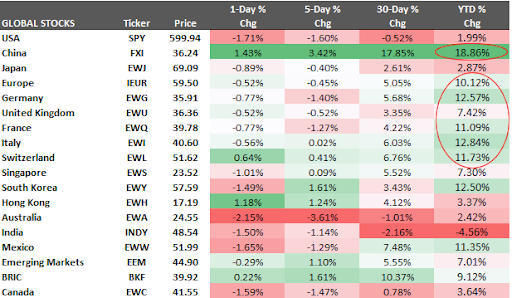

Adding to market anxieties, the U.S. market has underperformed its global peers since the inauguration.

Among G7 nations, the U.S. has posted the weakest returns, and its performance ranks near the bottom globally.

This divergence is particularly striking given the strong performance of Chinese equities, with the iShares MSCI China ETF (MCHI) registering a nearly 19% gain over the same period. This stark contrast between U.S. and Chinese market performance presents a puzzle that warrants closer examination.

Goldman Sachs has significantly revised its year-end gold price target to $3,100 per troy ounce, bolstering the bullish case for the precious metal.

The investment bank’s optimistic outlook is predicated on several key factors. Analysts anticipate stronger-than-previously-forecast central bank gold purchases and increased inflows into bullion-backed exchange-traded funds (ETFs). Furthermore, Goldman Sachs highlights the substantial hedging value offered by long gold positions, particularly in light of potential escalations in trade tensions.

Following a record high of $2,972 per troy ounce, gold prices have experienced a minor pullback to $2,950. This modest decline is likely attributable to profit-taking by short-term traders.

Source: TradingView

European natural gas futures have tumbled recently, driven by growing optimism surrounding potential peace talks between Russia and Ukraine. Speculation about a possible resolution to the conflict, particularly following reports of U.S.-brokered discussions, has raised hopes of resuming Russian pipeline gas flows to Europe, significantly easing supply concerns.

This shift in market sentiment has been a primary catalyst for the price decline.

The Dutch Title Transfer Facility (TTF) front-month futures, the benchmark contract for European gas, have fallen sharply since early February 2025, erasing more than 13% of their value from levels earlier in the month. This retreat follows a period of near two-year highs, fueled by the cessation of Russian gas transit through Ukraine as of January 1, 2025, cold weather forecasts, and increased competition for liquefied natural gas (LNG) imports.

Several other factors have contributed to the downward pressure on prices. European nations are reportedly considering easing mandatory gas storage refill targets for the upcoming season, potentially dampening demand for LNG. Weaker demand in Asia has also freed up additional LNG supplies for European markets.

Source: TradingView

Oil prices are currently navigating uncertainty, with several key decisions and geopolitical factors poised to influence market direction. A potential postponement of the OPEC+ production increase planned for April could provide price support, while developments in Ukraine and Iran add further complexity to the outlook.

April WTI crude has demonstrated resilience around the $70 per barrel mark, successfully defending this level on multiple occasions in recent trading sessions. The possibility of easing tensions in Ukraine, coupled with the administration’s stated intentions to de-escalate the conflict, suggests the potential for reduced or removed Russian sanctions. Simultaneously, the administration’s stance toward Iran could lead to new sanctions, potentially offsetting any relief from easing restrictions on Russia.

The upcoming OPEC+ meeting takes on added significance in this environment. Recent reports indicated that OPEC+ delegates were considering a further delay in restoring output, though this was subsequently denied by Russia. The group faces a delicate balancing act as it seeks to manage supply amidst fluctuating global demand and increasing production from non-OPEC+ nations.

Oh, degens, you’re not gonna believe this. Bybit exchange, bless their hearts; they just got absolutely wrecked. Like, “rug pulled on a cosmic scale” rekt.

A cool $1.4 BILLION in ETH vanished from their cold wallet. Poof. Gone. Like it never existed. Whoops.

This is a whale-sized hack, dwarfing Coincheck, Mt. Gox, and even FTX. We’re talking record-breaking levels of “oops, all my ETH.”

Bybit CEO Zhou tried to play it cool on X, saying withdrawals are “normal.” Yeah, normal for a multi-billion-dollar hack. He claims the hacker pulled some UI trickery, like a digital magic show, fooling their cold wallet signers into approving a malicious transaction. Think of it as a DeFi phishing scam on steroids. Apparently, the hacker used a fake Safe Wallet URL. Classic.

Despite the massive L, Zhou insists Bybit is solvent and will cover the losses. “Don’t worry, degens,” he probably said, “your funds are totally safe…ish.”

These performance charts track the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.