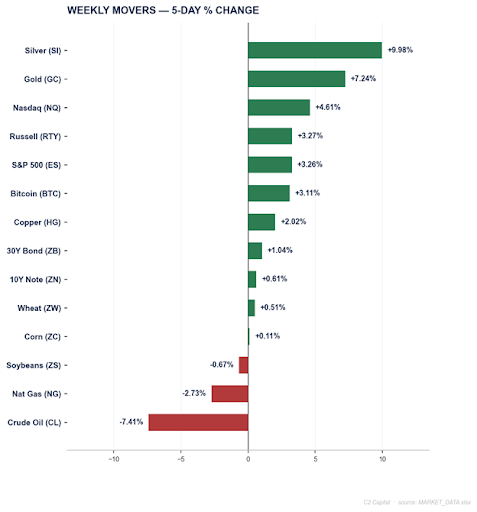

Week 33: The Great Decoupling — One Soft Jobs Print, Gold & Silver Ripping, Oil Reversing, and Bitcoin Nowhere

- Gold (GCQ26) ripped +7.24% to $4,339.20 and silver (SIU26) surged +9.98% to $63.39 on the week as July nonfarm payrolls unexpectedly fell -23,000 (vs. +80,000 consensus). TD Securities-flagged short-covering trigger levels ($4,222 and $4,300), and silver backwardation reportedly widened to $2.88/oz, the largest since the 1980s.

- WTI crude (CLU26) reversed hard, -7.41% to $77.98, as OPEC+ finalized a September +188,000 bpd increase on August 2 — completing the group’s full rollback of its voluntary 1.65 million bpd cuts — while reports of a developing US-Iran-Oman framework to de-escalate Strait of Hormuz tensions unwound the geopolitical risk premium; a surprise +2.5 million barrel EIA crude build compounded the move.

- ZNU26 bounced +0.61% to 108-21.5, still within 0.6% of its 52-week low, caught between Fed Chair Kevin Warsh’s hawkish 9-3 FOMC hold (year-end dot-plot median now 3.8%, up from 3.4%) and today’s weak jobs data reviving rate-cut odds — a genuine two-way fight into the August 12 CPI print.

- Bitcoin (BTCQ26) is this week’s outlier: +3.11% to $64,880 but capped below $65,145 resistance despite the identical weak-dollar backdrop that sent gold to its best week since January — a divergence some desks are calling the ‘Great Decoupling.’ Whale wallets added roughly 20,000 BTC since July 29, and spot ETFs logged four straight days of inflows.

Data as of August 7, 2026 12:15 pm CT

WEEK IN REVIEW: MACRO CONTEXT

The week’s defining event landed on Friday: July nonfarm payrolls fell by -23,000 (consensus +80,000), a stunning miss compounded by a combined 103,000 downward revision to the May and June reports; the unemployment rate ticked down to 4.1% only because labor-force participation slipped.

The US Dollar Index logged its worst weekly performance in roughly three months on the print. That single data point is rippling through the futures complex in four different directions. Precious metals read it as textbook dollar-debasement: gold (GCQ26) rallied +7.24% to $4,339.20 and silver (SIU26) surged +9.98% to $63.39, with TD Securities’ flagged CTA short-covering trigger ($4,222) and re-long trigger ($4,300) both cleared on the gold leg, and silver backwardation reportedly widening to $2.88/oz — the largest since the 1980s — as London vault metal struggles to meet delivery demand.

Crude oil told the opposite story from the same weak dollar. WTI (CLU26) fell -7.41% to $77.98 after OPEC+ confirmed on August 2 a final +188,000 bpd increase for September — completing the group’s full rollback of its voluntary 1.65 million bpd production cuts — while reports of a developing US-Iran-Oman framework to de-escalate Strait of Hormuz tensions further unwound the geopolitical risk premium built up earlier this year.

Rates are this week’s genuine tug-of-war: ZNU26 sits within 0.6% of its 52-week low after Fed Chair Kevin Warsh’s FOMC held rates at 3.50–3.75% on a hawkish 9-3 vote on July 29 — three dissents wanted an immediate hike, and the updated dot plot lifted the year-end median to 3.8% from 3.4% — but this morning’s weak jobs data clawed back some of that yield pressure, bouncing ZNU26 +0.61% on the week heading into the August 12 CPI print.

Bitcoin is this week’s outlier. BTCQ26 gained a modest +3.11% to $64,880 but could not clear $65,145 resistance despite facing the identical weak-dollar, weak-jobs backdrop that sent gold to its best week since January — a divergence some desks are calling the ‘Great Decoupling’ of digital and physical gold. Whale wallets (10–10,000 BTC cohort) added roughly 20,000 BTC (~$1.2B) since July 29, and spot BTC ETFs logged four consecutive days of net inflows (~$750–765M, led by BlackRock’s IBIT), but retail sentiment remains in ‘extreme fear '.

Data as of August 7, 2026 12:15 pm CT

PRECIOUS METALS (GCQ26 / SIU26) — DOLLAR-WEAKNESS RECHARGE; CTA TRIGGERS CLEARED

Gold and silver both reignited this week on a combination of positioning dynamics and genuine tightness in the physical market. Gold (GCQ26) gained +7.24% to $4,339.20 and silver (SIU26) surged +9.98% to $63.39 — both moves accelerating alongside London physical buying and algorithmic/CTA flow from multiple venues.

The catalyst was this Friday’s July jobs report (-23,000 vs. +80,000 consensus, with a 103,000 combined downward revision to May/June), which drove the Dollar Index to its worst weekly performance in roughly three months.

TD Securities had flagged $4,222 as gold’s CTA short-covering trigger and $4,300 as the level where systematic trend-followers re-establish net-long exposure — GCQ26 has now cleared both, mechanically confirming the ‘CTA money covering shorts’ dynamic.

PRICE ACTION & TECHNICAL STRUCTURE

GCQ26 settled through its prior resistance band, last at $4,339.20 (+7.24% on the week, +$292.95) after an intraday range of $4,277.00–$4,371.50. The former resistance level ($4,283.30) has been decisively cleared and now serves as the first support shelf on any pullback; price is above MA20 ($4,088.20) and MA50 ($4,183.50) but still below MA100 ($4,443.00) and MA200 ($4,553.90) — a partial MA-stack recovery, not yet a full bullish stack. GCQ26 sits 24.0% below its 52-week high of $5,706.00 — meaningful room remains before any ‘fresh high’ claim would apply.

SIU26 shows an even sharper acceleration: last $63.39 (+9.98%, +$5.75) on an intraday range of $61.86–$65.48, clearing its resistance shelf ($62.91) with volume of 53,727 contracts running at 1.50x the 20-day average (35,849) — confirmed, above-average participation on the breakout, not a thin-market spike. RSI 58.42 and ADX 25.15 both point to a trend with room left to run before overbought territory.

NOTABLE POSITIONING & FLOW

The relevant positioning signal is mechanical: TD Securities’ CTA trigger framework (gold covering above $4,222, re-longing above $4,300) has now been cleared by price, and the desk’s own caution — that a prior cycle saw gold run nearly $670/oz (20%) before triggering CTA profit-taking.

WATCH ITEMS

- Hot CPI (Aug 12): A headline or core print materially above consensus would revive the hold-to-hike debate inside Warsh’s FOMC — reduce conviction on a hot print.

- Silver backwardation resolution: If London vault flows normalize and the reported $2.88/oz backwardation compresses quickly, the physical-squeeze component of the silver thesis fades and the trade reverts to a pure CTA/dollar-beta story with lower conviction.

- Real yields breaking higher: 10-year real yields near 2.41–2.42% are already a headwind the rally is overcoming; a sustained move above 2.5% on hawkish repricing would remove one of the two supports (dollar weakness) underneath the metals bid.

CRUDE OIL (CLU26) — OPEC+ ROLLBACK COMPLETE; HORMUZ RISK PREMIUM UNWINDS

WTI crude (CLU26) reversed sharply this week, falling -7.41% to $77.98, as two separate supply-side developments unwound in the same five sessions. First, OPEC+ confirmed on August 2 a final +188,000 bpd increase for September — the group’s fifth consecutive monthly hike since April and the move that completes the full rollback of its voluntary 1.65 million bpd production cuts, removing lingering uncertainty about the pace of supply normalization. Second, reports that the US, Iran, and Oman are approaching a 60-day interim arrangement to de-risk the Strait of Hormuz further unwound the geopolitical risk premium built into prices earlier this year; the precise status of that framework remains fluid and is reported as ‘close to’ an agreement rather than signed. A surprise +2.5 million barrel EIA crude build for the week ended July 31 — contrary to consensus expectations of a draw — compounded the move, and preliminary API data for the following week (~+4.07M bbl) points to a second consecutive build. Today’s weak NFP print (-23,000 jobs) added a demand-destruction overlay on top of the supply story.

PRICE ACTION & TECHNICAL STRUCTURE

CLU26 last traded $77.98 on an intraday range of $76.53–$78.77, settling the prior session at $77.29. The 5-day decline of -7.41% (-$6.24) has pushed the price below MA20 ($81.63), MA50 ($79.03), and MA100 ($81.52) while remaining above MA200 ($71.36) — a bearish near-term MA stack sitting on top of a still-intact longer-term uptrend.

CLU26 sits 18.2% below its 52-week high of $95.30 and roughly 40.5% above its 52-week low ($55.49). Support sits at $75.07; a break there opens the MA200 zone ($71.36) as the next structural test.

FUNDAMENTAL THESIS

The Hormuz risk-premium unwind: a developing US-Iran-Oman framework to de-escalate Strait of Hormuz tensions (still fluid, not confirmed signed) is removing the geopolitical floor that had supported prices, consistent with the Brent-led selloff on August 4 specifically attributed to renewed US-Iran diplomacy hopes.

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- Confirmed US-Iran-Oman signing (primary risk): An actual signed Hormuz de-escalation framework — not just reported progress — would remove the last geopolitical floor and open a path toward $75 support and the MA200 cluster near $71–72. Conversely, a collapse in talks would rapidly restore the risk premium.

- Second consecutive EIA build (Aug 12): The API’s preliminary +4.07M bbl read for the following week suggests the Aug 12 official EIA print may confirm sustained demand softening — a build meaningfully above the 5-year seasonal average would reinforce the short thesis; an unexpected draw would flag the selloff as overdone.

- Break below $75.07 support: A confirmed close below support on above-average volume (current volume is running well below average, so a volume-confirmed break would be a meaningful signal) opens the MA200 zone near $71.36 as the next target.

10-YEAR T-NOTE (ZNU26) — WARSH'S HAWKISH HOLD VS. TODAY'S WEAK JOBS PRINT

ZNU26 bounced +0.61% to 108-21.5 this week, but remains within 0.6% of its 52-week low — a genuine two-way fight between a structurally hawkish Fed and a labor market that just cracked. Fed Chair Kevin Warsh — confirmed by the Senate 54-45 in the closest modern-era confirmation vote and sworn in May 22, 2026 — was appointed by President Trump explicitly seeking rate cuts, but has governed hawkishly since taking office.

At the July 29 FOMC meeting, the Committee held rates at 3.50–3.75% on a 9-3 vote, with three dissents (Hammack, Kashkari, Logan) favoring an immediate 25bp hike, and the updated dot plot lifted the year-end 2026 median to 3.8% — up sharply from 3.4% in March, meaning a hike is now the Committee’s own implied median path.

That backdrop had pressured ZNU26 to within 0.6% of its 52-week low. But this morning’s July jobs report — payrolls falling -23,000 (vs. +80,000 consensus) with a combined 103,000 downward revision to May/June — reintroduced rate-cut odds at 55.9% even against the hawkish dot plot, driving this week’s bounce.

PRICE ACTION & TECHNICAL STRUCTURE

ZNU26 last traded 108-21.5 against a prior settle of 108-16, a +0.61% weekly gain (+0-21). Price sits just below MA20 (108-22) and well below MA50 (109-07) and MA100 (109-26) — the medium-term MA stack remains bearish even after this week’s bounce. ZNU26 is trading within 0.6% of its 52-week low (107-31.5) and roughly 4.6% below its 52-week high (113-30). RSI at 47.15 and ADX at 15.25 (a weak trend reading) both point to a market in genuine consolidation rather than a resolved direction. Volume of 1,471,795 contracts ran at 0.83x the 20-day average (1,762,887) — solid institutional participation, not a thin, low-conviction bounce. The companion 30-year contract (ZBU26) confirms the same structure: +1.04% on the week, also trading within 1.1% of its own 52-week low (108-08) — the entire long end of the curve is coiling near cycle-low prices (cycle-high yields) awaiting the next data point. Support sits at 108-09.5; resistance at 108-27.

NOTABLE POSITIONING & FLOW

No single named ZN/ZB block trade for this specific week was identified via research — this positioning color should be read as thematic (record STIR/rates OI reflecting policy-path uncertainty), not a specific verified block print.

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- August 12 CPI (primary trigger): This is the resolution point for the entire setup. A hot print validates the FOMC’s hawkish dissenters and likely takes ZNU26 to a fresh 52-week low; a soft print extends the jobs-data-driven bounce toward MA20.

- Weak Treasury auctions (Aug 11-13): Softening foreign demand (Japan, China both reducing UST holdings this year) means a weak bid-to-cover on the $125B refunding slate, stacked directly on top of CPI/PPI week, would compound yield pressure independent of the inflation data itself.

- Jackson Hole on deck (Aug 27–29, outside this window): Chair Warsh’s keynote is traditionally the year’s most market-sensitive Fed moment; as of early August he described the speech as ‘a blank piece of paper’ — begin positioning for volatility around that date even though it falls outside the current 10-day catalyst window.

BITCOIN (BTCQ26) — THE ‘GREAT DECOUPLING’: CAPPED AT $65K WHILE GOLD RIPS

Bitcoin (BTCQ26) gained +3.11% to $64,880 this week, but the more important fact is what it did NOT do: clear $65,145 resistance, despite facing the exact same weak-dollar, weak-jobs backdrop that sent gold to its best week since January. Some desks are calling this divergence the ‘Great Decoupling’ — gold surged roughly 6.6–7% this week while BTC added under 1% over the same stretch, even though the trailing correlation between the two assets has been cited around 0.73.

PRICE ACTION & TECHNICAL STRUCTURE

BTCQ26 last traded $64,880, up +3.11% (+$1,956.91) on an intraday range of $64,290–$66,020. Price is coiling right at the MA20/MA50 cluster ($64,735 / $64,485) and well below MA100 ($70,264) — a near-term MA stack that has flattened out rather than confirming a clean uptrend.

BTCQ26 sits 22.9% below its 52-week high ($84,165) and 11.6% above its 52-week low ($58,115).

The broader structural level map — support at $58–59K and $63K, resistance at $67K, $69K, and $71K: A hold above $67K would favor a retest of $71K; a loss of $63K favors reversion toward $58K; a loss of $58–59K opens room for a significantly larger decline.

FUNDAMENTAL THESIS

Two forces are pulling in opposite directions. On the constructive side: whale wallets (the 10–10,000 BTC cohort) added roughly 20,000 BTC (~$1.2B) since July 29 even as smaller/retail holders reduced exposure — a divergence Santiment reads as raising the odds of a push through $70K and lowering the odds of a break below $60K. Spot BTC ETFs logged four consecutive days of net inflows (~$750–765M total), with BlackRock’s IBIT responsible for roughly three-quarters of the flow, and CME BTC futures open interest jumped +6.82% in a single day to $6.66B (102,840 BTC) — consistent with larger desks rebuilding exposure.

On the negative side: a Coldcard hardware-wallet firmware vulnerability (dating to a 2021 release) has drained an estimated $89–130M from self-custody wallets since July 30, a headline that is denting retail confidence even though it is a wallet-specific exploit, not a protocol or exchange failure. Mining difficulty fell 0.74% to 126.23T at the July 25 adjustment — now roughly 1.1% below year-ago levels, only the second year-over-year decline in Bitcoin’s history — reflecting weak hashprice economics near or below breakeven amid AI/HPC power competition for electricity. Perhaps most importantly for the 'decoupling' thesis:

NOTABLE POSITIONING & FLOW

Deribit options skew has flipped decisively bearish, with the $60,000 put now the single most crowded strike (roughly $1.17B notional open interest per one source) — a reversal from the $70K/$72K calls (each ~$2.5B OI) that dominated positioning just before the FOMC. That combination — constructive flows, defensive options — is consistent with a market that wants to believe in upside but is paying up to hedge the downside first.

WATCH ITEMS

- Decisive close above $65,145/$67K: A confirmed close above the technical resistance and then the structural $67K level would open a path to retest $69K and $71K — the level the user’s framework flags as the key upside pivot.

- Loss of $63K: A break below the $63K structural support (well above the tighter $64,205 technical support) would favor reversion toward the $58–59K zone; a further loss of $58–59K opens room for a significantly larger decline per the user’s own framework.

- Deribit put-skew unwind: If the $60K put open interest is unwound (traders taking profits on the hedge or letting it roll off) without a corresponding price decline, that would be a genuinely bullish signal — it would suggest the hedging flow, not spot conviction, has been the binding constraint on price.

IMPORTANT NOTICE — PLEASE READ CAREFULLY

This publication is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any futures contract. Futures trading involves substantial risk of loss and is not appropriate for all investors; leverage can work against you as well as for you. Past performance is not indicative of future results. Per CFTC Rule 4.41, any hypothetical or simulated performance results have inherent limitations, do not represent actual trading, are prepared with the benefit of hindsight, and no representation is made that any account will achieve similar profits or losses.

Week 32: War Premium Digests, Fed Holds the Line, and Market Rebalances Post Hedge Fund Liquidation Shock

- CLU26 pulled back to $83.59 as of writing (-5.36% week) from last week's $92 geopolitical peak; the MA-stack bull structure is intact (above all four moving averages) and EIA confirmed a -7.167M bbl crude draw for the week ending July 24 — demand is absorbing the war premium even as the Houthi maritime embargo on Saudi Arabia extends the supply disruption story.

- ZNU26 printed a fresh 52-week low at 108-02 (just above the 108-00 prior floor) after the FOMC voted 9-3 to hold at 3.50–3.75%; three dissenters demanded a rate hike, signaling that oil-driven inflation from the US-Iran conflict has eliminated the rate-cut runway.

- ESU26 recovered to settle $7,514 as of writing (within reach of its 52-week high) as Microsoft delivered a blowout quarter ($90B revenue, Azure +43%, Azure crossing $100B in annual run-rate) that validates the AI monetization thesis; the FOMC relief rally and tech earnings recovery position ES for a run at the $7,693.75 52-week high if August macro data cooperates.

- The Senate shelved the CLARITY Act until at least September, prioritizing Russia sanctions and federal nominations; BTC (BTCQ26) see-sawed on the Fed hold at $65,085 settle before recovering above $64,000 on Thursday as tech stocks rallied — the legislative catalyst is deferred, not dead.

- Corn (ZCZ26) slid -5.38% to 462.00¢ despite a crop ratings drop to 63% G/E (down 4pp) during the critical pollination window; the August 12 WASDE will be the first structural re-price of the weather premium — watch CPC 8–14 day outlooks for heat-dome persistence as the next catalyst for a ZC recovery trade.

Data as of 12:00 pm CT July 31, 2026.

WEEK IN REVIEW: MACRO CONTEXT

KEY TAKEAWAYS

The week delivered a trifecta of macro events that reshuffled tactical positioning across energy, rates, and equities.

The Federal Reserve held interest rates unchanged at 3.50–3.75% on Wednesday, July 29, in a 9-3 vote — but the three dissents were hawks, not doves. Fed Chair Kevin Warsh stopped short of signaling an imminent hike, but the message embedded in three dissenting votes was clear: oil-driven inflation from the ongoing U.S.–Iran war has reduced the Fed’s tolerance for accommodation and eliminated the rate-cut runway.

WTI crude (CLU26), which surged to $92.19 last week on the two-chokepoint thesis, pulled back to settle $83.59 on July 31 (-5.36% week) as traders managed geopolitical exposure and OPEC+ supply increments absorbed some of the shock. But the pullback is structural digestion, not thesis invalidation: the U.S. military struck Iranian naval targets on July 29, Houthi forces declared a maritime embargo on Saudi Arabia, and the EIA reported a -7.167M-barrel crude draw for the week ending July 24 — confirming demand remains intact despite the price spike.

Equity markets absorbed the week’s uncertainty and rallied on the back of a decisive tech earnings beat. Microsoft reported Q4 FY2026 revenue of $90.0B (+18% YoY) with Azure growing +43%, crossing $100B in annual run-rate revenue for the first time — the first hyperscaler to demonstrate that AI capex is converting to revenue at scale. ESU26 gained +0.74% on the week to $7,514 as of writing, recovering from the prior week’s Alphabet-and-Tesla-driven selloff. Meta reported a more complex story: revenue +28% to $60.8B but EPS of $6.18 missed the $7.22 consensus as expenses surged 55% to $42B. The market absorbed Meta’s miss because Microsoft’s Azure inflection provided a credible AI ROI counterpoint.

Data as of 12:00pm CT July 31, 2026.

CRUDE OIL (CLU26) — WAR PREMIUM DIGESTS TO $83; MA-STACK BULL INTACT

WTI crude (CLU26) delivered a classic post-spike digestion week: after surging +8.14% to $92.19 on the two-chokepoint thesis, this week’s -5.36% pullback to $83.59 represents profit-taking and headline-fatigue rather than a structural thesis reversal.

CLU26 is trading above all four key moving averages (20/50/100/200-day); the MA stack that underpins the bull regime is unbroken, and the EIA’s -7.167M barrel crude draw for the week ending July 24 — the largest draw of the year — confirmed that physical demand is absorbing barrels even at elevated price levels.

The Houthi maritime embargo on Saudi Arabia, declared this week, and ongoing Strait of Hormuz incidents mean the supply-disruption risk floor remains structurally in place.

Dip buyers between $82–84 are operating with defined support ($82.39), and a clear catalyst pipeline: EIA on August 5 and continuing war news flow are the primary price movers.

PRICE ACTION & TECHNICAL STRUCTURE

The 5-day price decline of -5.36% (-$4.74) is technically healthy: the entire pullback occurred above all four moving averages (MA20: $80.04; MA50: $80.08; MA100: $81.58; MA200: $70.88), meaning sellers have not broken the structural bull trend. RSI at 55.86 is mid-range — not overbought, not signaling capitulation — consistent with orderly profit-taking rather than a momentum reversal. Key support is $82.39; resistance is $85.36 (the current ceiling that capped the last two intraday rallies). The prior session high ($95.30 = 52-week high) remains the ultimate target if the two-chokepoint thesis escalates. The $80–82 MA cluster zone is a structural loading area for tacticians who missed the initial entry.

Seasonal Note: WTI historically maintains a late-summer demand premium through August (driving season demand peak, pre-autumn refinery maintenance), but in 2026 the geopolitical risk premium from the US-Iran conflict dominates any seasonal signal — directional moves are headline-driven, not seasonally predictable.

NOTABLE BLOCK TRADES & OPTIONS ACTIVITY

CLU26 volume of 185,561 (rvol 0.66) reflects reduced speculative activity on the pullback week — a constructive sign. The options market is showing bifurcated institutional positioning: call spreads targeting the $88–92 zone (a reload trade for a second chokepoint escalation) are active, alongside put spreads at $80–82 (protection against a rapid de-escalation scenario).

The asymmetry favors upside: a coordinated Hormuz + Houthi de-escalation would need to be comprehensive and verified to push crude below $80, whereas any single chokepoint incident can reprice $90+ within hours.

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- Coordinated de-escalation (primary risk): Any simultaneous Hormuz ceasefire AND Houthi suspension of Saudi maritime attacks would collapse the war premium by $8–12 within hours. A single-front ceasefire (either Hormuz or just Houthi) would modestly compress prices but not break the structural bull. Monitor for a joint U.S.–Iran announcement or UN-mediated deal; current ceasefire mediator talks are targeting a 10-day truce.

- EIA August 5 (secondary): The prior -7.167M bbl draw sets a high bar. A crude build >+3M bbl or a Cushing build >+2M bbl would signal demand-side softening at elevated prices — reduce CL long on a large, unexpected build.

- Break below $82.39 support: If CLU26 closes below $82.39 on above-average volume, sellers have broken the first MA support layer; next support is the MA cluster at $80. A close below $80 invalidates the bull thesis entirely — exit long exposure.

10-YEAR T-NOTE (ZNU26) — FRESH 52-WEEK LOW; HAWKISH-HOLD LOCKS YIELD PRESSURE

ZNU26 (September 10-Year Treasury Note) printed a fresh 52-week low at 108-02 this week, barely above the prior 52-week low floor at 108-00. The move lower was the direct consequence of the FOMC’s July 29 hawkish hold: a 9-3 vote to leave rates unchanged, with three Federal Reserve bank presidents dissenting in favor of an immediate 25-basis-point rate hike.

Fed Chair Warsh declined to signal whether a hike is forthcoming, but the dissent count itself is the message: oil-driven inflation from the U.S.–Iran war has created a live debate inside the FOMC about whether rates need to move higher, not lower.

In a world where three of twelve voting members are hawkish enough to vote for an immediate hike, the Treasury market is correctly pricing out rate cuts and beginning to price in rate-hike risk. RSI at 36.18 is approaching oversold territory, creating a short-term squeeze risk ahead of the August 7 NFP, which will deliver the next directional catalyst.

PRICE ACTION & TECHNICAL STRUCTURE

ZNU26 settled at 108-17.5 on July 31 with a session low of 108-02 — the intraday low established a fresh 52-week low (prior 52-week low: 108-00). The MA stack is decidedly bearish: ZNU26 trades below MA20 (108-26.5), MA50 (109-08.5), and MA100 (109-30.5), with each moving average acting as a rolling resistance layer on bounces.

The range between support (108-09) and resistance (108-23.5) is tight: ZN is coiling just above its 52-week floor, creating a setup where a break below 108-00 could accelerate toward 107-16 on institutional stop-running, while a bounce off 108-00 support could push back toward MA20 (108-26.5) on any dovish data surprise.

FUNDAMENTAL THESIS

The Treasury market is now pricing the ‘oil-driven inflation trap’ thesis: the Fed cannot cut rates while WTI is above $80 and CPI is being supported by energy costs; it cannot credibly hike into a late-cycle economy without risking a demand shock. The FOMC’s 9-3 vote — with dissenters Cleveland Fed (Beth Hammack), Minneapolis Fed (Neel Kashkari), and Dallas Fed (Lorie Logan) all favoring a hike — signals that the hawkish threshold has been met for a meaningful minority of the committee.

The market is now pricing in approximately 60% odds of at least one hike by September (per CME FedWatch), a material shift from the near-zero probability priced three weeks ago.

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- Break below 108-00 (primary trigger): A confirmed settle below the 52-week low (108-00) on above-average volume signals that institutional sellers are committed and stops are being run — target 107-16 to 107-00. This is the structural short trigger and requires strong NFP (August 7) or hot CPI (August 12) as the catalyst.

- NFP August 7 weak print (squeeze risk): If July employment shows <100K nonfarm payrolls or unemployment rises to 4.5%+, the market will aggressively unwind rate-hike pricing and ZN will short-squeeze toward MA20 (108-26.5) and potentially MA50 (109-08.5).

- RSI oversold bounce (<30): If RSI falls below 30 before NFP, a mechanical mean-reversion bounce is likely regardless of fundamentals — especially on a thin August Friday ahead of the long weekend. Size positions accordingly and hold stops above 108-23.5.

S&P 500 E-MINI (ESU26) — AZURE CROSSES $100B; FOMC RELIEF RALLY INTACT

ESU26 recovered +0.64% on the week to $7,514, now trading within 2.4% of its 52-week high of $7,693.75 — a meaningful rebound from last week’s post-Alphabet/Tesla selloff.

The catalyst for the recovery was Microsoft’s Q4 FY2026 earnings: $90.0B in revenue (+18% YoY), Azure growing +43%, and Azure’s first crossing of $100B in annual run-rate revenue. This is the proof of concept the AI investment community had been waiting for — the first hyperscaler to demonstrate that AI capex is converting into enterprise revenue at scale.

PRICE ACTION & TECHNICAL STRUCTURE

The +0.74% weekly gain masked a volatile week: the index was as low as $7,369 early in the week before FOMC relief and Microsoft earnings drove the recovery. Current price ($7,514 last) sits below MA20 ($7,521.02) and MA50 ($7,529.71) but well above MA100 ($7,281.34) and MA200 ($7,138.17), positioning ESU26 in a medium-term bull trend with short-term price compression.

RSI at 49.82 is precisely neutral — no directional momentum signal either way, consistent with a market waiting for the next macro catalyst. The technical setup is a coil just below the MA20/MA50 cluster: a close above $7,536.67 (resistance_1) on above-average volume would confirm a breakout toward the 52-week high ($7,693.75); a close below $7,369.67 (support_1) would signal the FOMC/earnings relief is fading and the prior AI-capex selloff is resuming.

NOTABLE BLOCK TRADES & OPTIONS ACTIVITY

ESU26 realized vol remains elevated following the Alphabet/Tesla selloff week, with put skew at 7,300–7,400 still elevated (gamma zone protection from last week is being rolled up to 7,400–7,450 following the recovery). The significant shift this week is call activity at 7,600–7,650: institutional positioning for a run at the 52-week high ($7,693.75) on a strong August 7 NFP print.

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- Close above $7,536.67 (resistance_1) on volume: A confirmed settle above resistance would confirm the MA20/MA50 cluster has been cleared and the path to the 52-week high ($7,693.75).

- NFP August 7 ‘too hot’ scenario: A blowout print (>250K, unemployment below 4.0%) would revive rate-hike expectations and compress ES multiples despite strong economic growth — exit long exposure if ES sells off below $7,370 on the NFP session.

- Oil above $90 sustained: If CLU26 recovers to $90+ on fresh geopolitical escalation, the stagflation narrative reactivates — energy costs compress discretionary spending and the Fed moves closer to a hike. That scenario is ES-negative and would likely push the market back to the $7,369 support zone.

SIDELINED MARKETS

IMPORTANT NOTICE — PLEASE READ CAREFULLY

This publication is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any futures contract. Futures trading involves substantial risk of loss and is not appropriate for all investors; leverage can work against you as well as for you. Past performance is not indicative of future results. Per CFTC Rule 4.41, any hypothetical or simulated performance results have inherent limitations, do not represent actual trading, are prepared with the benefit of hindsight, and no representation is made that any account will achieve similar profits or losses. This document is confidential, intended solely for the recipient, and may not be redistributed. © 2026. All rights reserved.

Week 31: Two Chokepoints, a Gamma Cliff, and a Senate Bill — Geopolitics and Positioning Risk Drive Four Distinct Setups

KEY TAKEAWAYS

- CLU26 surged +8.14% to make high around $92.19 on Thursday as the two-chokepoint thesis went live: the Strait of Hormuz (Iran naval confrontation) and Bab-el-Mandeb (Houthi attacks on Saudi tankers, Jul 22–23) both activated simultaneously; WTI dipped to $88.29 (last) on Jul 24 — the $88–90 dip zone our analysts identified as a place to play.

- ESU26 slipped -1.26% on Jul 23 to settle at $7,445 ($7473 Friday at writing) after Alphabet (-7%) and Tesla (-15%) earnings triggered an AI-capex re-rating; SpotGamma dealer gamma support thins materially below 7,300 — the tactical short pivot.

- GCQ26 gained +1.29% to $4,050 settle (last $4,070) while SIU26 surged +4.73% to $58.05; the metals complex is building a squeeze setup at RSI 45 — not yet oversold — supported by PBOC’s 20th consecutive month of gold purchases (14.93 tonnes, June 2026).

- CME BTC futures (BTCQ26) at $64,205 as of writing face a no-date binary: the Senate CLARITY Act is stalled on a Democrat ethics impasse; a cloture motion filing would catalyze a $70K+ response; failure to advance is a near-term overhang.

- FOMC July 28–29 (hold expected; Warsh statement 2:00 PM ET Jul 29) sets the cross-asset tone; July 30 delivers a compressed triple stack at 8:30 AM ET — GDP Q2 advance, PCE June, and USDA Export Sales — one day after the rate decision.

Data as of 12:05 pm CT July 24, 2026.

WEEK IN REVIEW: MACRO CONTEXT

The week was shaped by a thesis that moved from speculation to structural reality: both of the world’s critical oil export chokepoints came under simultaneous attack. The Strait of Hormuz — through which approximately 20% of global seaborne crude transits — remained contested under the ongoing U.S.–Iran confrontation. On July 22–23, Houthi forces escalated in the Red Sea, deploying missiles and drones near Bab-el-Mandeb and striking two Saudi National Shipping Company tankers. Saudi Arabia temporarily suspended Red Sea crude exports in response. With both export arteries under simultaneous threat, CLU26 (September WTI) settled at $92.19 on July 23 — a +8.14% five-session gain — before pulling back to $88.29 intraday on July 24 as traders managed exposure ahead of the weekend.

Simultaneously, equity futures absorbed a significant re-rating. Alphabet reported Q2 earnings on July 22, beating on revenue but announcing 2026 AI infrastructure capex guidance of $195–205B (above the $180–190B consensus). The market interpreted this as a signal that monetization timelines for AI infrastructure are extending faster than capex cycles, triggering a 7% single-session decline in Alphabet. Tesla (-15%) and Meta (-3.4%) compounded the damage.

Gold and silver quietly built their base: GCQ26 gained +1.29% to settle at $4,050 while SIU26 surged +4.73% to $58.05, both supported by the geopolitical safe-haven bid and a PBOC that has now bought gold for 20 consecutive months.

CME Bitcoin futures (BTCQ26) held near $64,205 as of writing— the market’s attention fixed on the Senate CLARITY Act, where Democrat opposition has stalled a floor vote and created a binary legislative catalyst with no scheduled date.

Data as of 12:05 pm CT July 24, 2026.

CRUDE OIL (CLU26) — TWO-CHOKEPOINT SURGE: KEY LEVEL AT $88–90

WTI crude oil (CLU26) is the week’s defining macro story — the two-chokepoint thesis that flagged as a tail risk has become the operative market structure. With both the Strait of Hormuz and Bab-el-Mandeb simultaneously under kinetic threat, the 20% of global seaborne crude that passes through one or both corridors is now subject to a structural risk premium that OPEC+ supply growth cannot fully offset.

PRICE ACTION & TECHNICAL STRUCTURE

CLU26 settled at $92.19 on July 23 (session high $92.83, low $87.68), marking the +8.14% five-session surge driven by the two-chokepoint activation. Volume at 267,737 contracts ran at 114% of the 20-day average (234,713) — rvol of 1.14 confirms institutional participation behind the move, not a thin-market spike.

Technical structure is firmly bullish: ADX at 35.95 with DI+ (35.95) overwhelming DI- (8.58) confirms strong directional trend. RSI at 65.44 has room before reaching overbought territory. Price trades above all four MAs by a wide margin (MA20: $76.56; MA50: $80.94; MA100: $80.98; MA200: $70.31). Resistance at $94.69; 52-week high at $95.30 represents the next major ceiling.

NOTABLE BLOCK TRADES & OPTIONS ACTIVITY

CLU26 realized volatility rank at the 100th percentile flags an extreme regime for options pricing. Institutional paper flow is concentrated in two structures: near-dated call spreads targeting the $94–97 zone (capturing the chokepoint premium through month-end) with put protection bought at $84–85 (de-escalation hedges). The asymmetry is notable — the upside surprise if the Saudi Red Sea suspension extends is a move toward $95+ while a coordinated ceasefire on both fronts could rapidly compress the premium by $8–12. Volume at 1.14x the 20-day average across five sessions confirms this is a broad institutional repositioning rather than a speculative spike.

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- Coordinated de-escalation (primary): Any U.S.–Iran ceasefire AND Houthi suspension of Red Sea attacks simultaneously would collapse the geopolitical premium by $8–12 within hours — this is the tail risk that most undermines the thesis.

- EIA July 29 inventory (secondary): A crude build >+2M bbl or Cushing build >+1M bbl signals demand weakness penetrating the geopolitical overlay — reduces conviction to 3/5; a large draw (>-4M bbl) confirms demand resilience and supports $94–97 extension.

- Break below $87.68 (session low): Structural support at $88.51 is close to current last price ($88.29); a clean break below $87.68 (today’s low) with volume signals de-escalation expectations are building — exit or reduce long exposure immediately.

S&P 500 E-MINI (ESU26) — TECH EARNINGS TRIGGER GAMMA ZONE APPROACH

The S&P 500 E-Mini (ESU26) is presenting a rare configuration: near its 52-week high (within 2.9% at $7,473.50 last) but with deteriorating internal momentum. Alphabet, Tesla, and Meta earnings triggered a momentum reversal on July 23 — the AI capex re-rating that the market had partially anticipated but whose magnitude (-7% Alphabet, -15% Tesla) still compressed risk appetite.

PRICE ACTION & TECHNICAL STRUCTURE

ESU26 settled at $7,445.00 on July 23 (down -1.26% on the session), with the session low at $7,431.50 breaching the prior support zone briefly before recovering intraday. Today (July 24), ESU26 is trading at $7,473.50 last — bouncing from oversold conditions but volume at only 69% of the 20-day average (rvol 0.69), suggesting the recovery is short-covering rather than a new-money bid.

The technical structure is decisively short-biased at the medium-term level: price sits below MA20 ($7,537.21) and MA50 ($7,536.23), while ADX at 10.24 with DI- (23.17) commanding DI+ (10.24) confirms directional selling pressure. RSI at 46.61 is approaching the mid-range without yet triggering an oversold bounce setup — there is room to fall to 40 before a mechanical reversal signal fires.

ATR at $89.66 means a 1.5R move from resistance ($7,525.75) to target would reach approximately $7,391 to $7,300 — the gamma zone. The 52-week low at $6,401.75 provides perspective on how much structural support exists below the current range.

NOTABLE BLOCK TRADES & OPTIONS ACTIVITY

ESU26 realized volatility rank is at the 74th percentile — elevated but not yet at extreme levels, suggesting options premiums are fair rather than richly priced. Put activity has increased notably following the Alphabet and Tesla earnings drops, with institutional hedging concentrated at 7,300–7,400 puts (protection against the gamma zone break) and 7,200 puts (tail hedge against a more decisive selloff). The key structural observation: put skew at the 7,300 strike is elevated relative to historical norms, suggesting the market is pricing in a non-trivial probability of reaching the gamma zone.

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- Microsoft and Meta earnings (week of Jul 27): Strong AI capex ROI narrative from remaining hyperscalers would partially reverse the Alphabet/Tesla selloff — look for ESU26 to reclaim MA20 ($7,537) on a positive earnings surprise. Thesis is invalidated if ES closes above $7,537 on volume.

- FOMC dovish pivot (Jul 29): A Warsh statement suggesting rate cuts are back on the table for September would send ESU26 above MA20 in the post-announcement session — exit short exposure immediately on any close above $7,537.

- 7,300 gamma break: If ESU26 breaches $7,300 on volume, dealer hedging flows flip from cushioning to amplifying the decline — this is the trigger for a potential 1–2% acceleration toward $7,200–7,254 (MA100); increase short conviction to 4/5 on a confirmed close below $7,388 (support_1).

GOLD (GCQ26) — METALS SQUEEZE SETUP BUILDING: PBOC FLOOR + FOMC BINARY

Gold (GCQ26) and silver (SIU26) are building a squeeze setup that our analysts have been monitoring: both contracts are in structural corrections from their 2026 peaks, both carry strong central-bank demand floors, and both are approaching technical levels where short positioning becomes crowded and RSI approaches but has not yet reached oversold.

PRICE ACTION & TECHNICAL STRUCTURE

GCQ26 traded at $4,070.10 (last) against a prior settle of $4,050.20, building on a +1.29% weekly gain that followed the prior week’s -2.2% correction. GCQ26 remains below all four moving averages (MA20: $4,077.30; MA50: $4,276.50; MA100: $4,550.30; MA200: $4,560.90), confirming the structural downtrend from the January 2026 all-time high. ADX at 15.37 with DI- (23.78) leading DI+ (15.37) indicates sellers retain structural control, but the trend is weakening (ADX below 20 signals indecision, not strong momentum). SIU26 at $58.95 last is testing its MA20 ($59.17) from below — a close above MA20 in silver would be the first momentum confirmation. Gold support at $4,013.80; resistance at $4,115.30.

FUNDAMENTAL THESIS

Three forces are in active tension for gold. The structural demand floor: China’s PBOC added 14.93 tonnes in June 2026, extending its gold-buying streak to 20 consecutive months and representing its largest single-month purchase since 2023. This provides a non-discretionary bid that has prevented deeper correction despite elevated real yields. The primary headwind: the 10-year Treasury yield near 4.57% (post-CPI-miss level) with core inflation at 2.6% YoY implies a real yield near +2%, raising the opportunity cost of holding non-yielding bullion. The squeeze catalyst: the June CPI surprise (-0.4% MoM, largest monthly drop since April 2020) removed near-term rate-hike risk and shifted expectations toward H2 2026 rate cuts. Silver’s +4.73% outperformance this week is significant — silver has historically led gold in squeeze initiations due to its higher beta and smaller open interest, and managed-money short positioning in silver is elevated near the 70th-80th percentile (compression fuel for a short cover rally).

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- CONTRACT ROLL GCQ26 first notice is July 31 (next Thursday). Traders holding long exposure must either close GCQ26 or roll to GCZ26 before that date to avoid delivery risk. The roll spread (GCQ26 vs. GCZ26 Dec) is the execution cost.

- SIU26 MA20 close confirmation ($59.17): Silver closing above its 20-day moving average would be the squeeze activation signal — follow-through in gold (GC) to $4,115 resistance becomes higher probability. Monitor silver as the leading indicator.

- Break below $4,013.80 support: A confirmed close below support on volume would invalidate the squeeze thesis and open a path toward $3,940–3,980; exit long positions and re-evaluate after FOMC catalysts clear.

BITCOIN CME (BTCQ26) — CLARITY ACT BINARY: LEGISLATIVE RISK WITHOUT A DATE

CME Bitcoin futures (BTCQ26) present a genuinely distinct setup from the other three featured contracts: a legislative binary event with an unscheduled trigger. The Senate CLARITY Act — the Digital Asset Market Structure legislation that cleared the Banking Committee 15-9 on May 14 — has stalled on the Senate floor as Democratic members objected to the removal of an ethics provision targeting presidential crypto profits. This is not a market risk in the conventional sense; it is a regulatory risk that determines whether the U.S. crypto market operates under a coherent legal framework or remains in enforcement-action limbo.

PRICE ACTION & TECHNICAL STRUCTURE

BTCQ26 settled at $65,095 on July 23 (range $63,930–$66,115 intraday) before pulling back to $64,205 on July 24 (last). The -0.44% weekly performance belies the binary risk embedded in the legislative outlook. Technical structure is mixed: BTCQ26 trades above its MA20 ($63,571) but below MA50 ($67,315) and MA100 ($71,117), placing it in a medium-term downtrend with short-term stabilization.

FUNDAMENTAL THESIS

The CLARITY Act legislative history: The Digital Asset Market CLARITY Act passed the Senate Banking Committee on May 14, 2026 (15-9), with two Democrats (Senators Hickenlooper and Cortez Masto) providing the votes for committee passage. However, three key Democrats (Senators Murphy, Van Hollen, and Merkley) formally opposed the bill after Republicans released a merged draft that omitted the ethics provision prohibiting a sitting president from holding crypto assets that benefit from legislation they sign. As of July 22, Republicans updated the bill to include a provision banning federal officials from issuing digital assets, but Democrats indicated the replacement language did not address their core ethics concern. The bill remains on the Senate Calendar (No. 423) without a cloture filing. The math: 60 votes needed to clear the filibuster; Republicans hold 53 seats; 7–9 Democratic votes are required; those votes are not secured. The binary: a cloture motion filing and successful vote would provide the U.S. crypto market with a clear legal framework, removing the enforcement-action discount embedded in BTC and ETH prices — estimated $8,000–$12,000 upside at minimum based on the market’s pre-uncertainty premium. Failure or indefinite delay means the existing enforcement-led regulatory posture continues.

NOTABLE BLOCK TRADES & OPTIONS ACTIVITY

CME BTCQ26 open interest at 8,472 contracts with rvol at 1.25x suggests modestly elevated positioning relative to recent history. Options activity on CME Bitcoin products shows a bifurcated skew: put protection at $58,000–60,000 (legislative failure hedges) is elevated versus call buying at $70,000–75,000 (cloture success positioning). Without a filing, BTCQ26 is range-bound $63,930–$66,180 until a legislative development forces a directional move.

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- Senate Majority Leader cloture filing: The single most important BTC signal of the week. Any announcement of a cloture motion filing moves BTC immediately. Without a filing, BTCQ26 will remain range-bound $63,930–$66,180.

- Democrat vote commitments: Public statements from Senators Murphy, Van Hollen, or Merkley indicating they will support or oppose the revised ethics provision are the secondary signal. Any indication that 7+ Democrats have committed to cloture = enter long BTCQ26.

- Break below $64,450 support on volume: A close below support signals legislative pessimism is hardening, and short positioning is building; reduces thesis to 1/5, move to Sidelined. Next support at $61,000–$62,000 then the $58,115 52-week low.

COMPLIANCE & DISCLAIMER

IMPORTANT NOTICE — PLEASE READ CAREFULLY. This publication is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any futures contract. Futures trading involves substantial risk of loss and is not appropriate for all investors; leverage can work against you as well as for you. Past performance is not indicative of future results. Per CFTC Rule 4.41, any hypothetical or simulated performance results have inherent limitations, do not represent actual trading, are prepared with the benefit of hindsight, and no representation is made that any account will achieve similar profits or losses. Specific entry, stop, and target levels are published separately in companion This document is confidential, intended solely for the recipient, and may not be redistributed. © 2026. All rights reserved.

Week 30: Summer Trade, Iran Reignites, Wheat Defies the Season — Geopolitical and Supply Shocks Rewrite the Commodity Playbook

KEY TAKEAWAYS

- CLQ26 surged +14.9% over five sessions — crude oil's largest weekly gain since the original Iran conflict spike — as US-Iran Strait of Hormuz attacks re-escalated July 13; OPEC+ August output hike (+188K bpd) provides a structural supply cap near $85.

- ZWU26 settled at 680.75¢, within 2.8% of its 52-week high (700.00¢), as USDA forecast the smallest U.S. winter wheat crop since 1965 (1.048 Bn bu, −25% YoY); CPC 6-10 day outlook extends below-normal precipitation across the Great Plains through late July.

- June CPI surprised sharply lower at −0.4% MoM (consensus: −0.1%) — the largest monthly decline since April 2020 — as energy deflation from the prior ceasefire washed through the basket; core CPI fell to 2.6% YoY, removing near-term rate-hike risk.

- GCQ26 is defending the $4,000 psychological floor (-2.2% week), trading below all four moving averages (20/50/100/200-day); China's central bank bought gold for a 20th consecutive month (14.93 tonnes in June); July 28–29 FOMC is the next major catalyst.

- FOMC July 28–29 is a HOLD consensus, but Fed Chair Warsh's post-meeting language on the rate path will be decisive across energy, rates, gold, and FX into August.

Data as of 11:35 am CT July 17, 2026.

WEEK IN REVIEW: MACRO CONTEXT

The week delivered two colliding macro shocks that split futures markets into distinct narratives. First, US-Iran Strait of Hormuz attacks re-escalated on July 13, reversing the June ceasefire narrative and sending CLQ26 (August crude) surging +14.9% over five sessions — the contract's largest weekly gain since the original conflict spike in March. Second, the June CPI print on July 14 shocked markets with a −0.4% monthly decline (vs. consensus −0.1%), the steepest monthly drop since April 2020. Energy deflation during the prior ceasefire period drove the headline, while core CPI fell to a flat 0.0% MoM (YoY: 2.6% vs. 2.8% prior), effectively eliminating near-term Federal Reserve rate-hike risk.

The same geopolitical event that had temporarily cooled inflation in June was now re-igniting energy prices in real time — creating a split-screen macro environment heading into the July 28–29 FOMC meeting.

Against this geopolitical backdrop, CBOT SRW Wheat (ZWU26) maintained its own independent structural rally, advancing +6.1% to settle at 680.75¢ — within 2.8% of its 52-week high. The driver: USDA's historic downgrade of U.S. winter wheat production to 1.048 billion bushels, the smallest crop since 1965, with hard red winter wheat (Plains region) down 36% year-over-year. Australia simultaneously cut its 2026 wheat harvest projection by 30%, removing a key export competitor.

Gold (GCQ26) oscillated near the $4,000 psychological floor, posting a -2.2% weekly loss as hawkish Federal Reserve rhetoric from Chair Kevin Warsh clashed with the dovish CPI surprise. China's central bank extended its gold-buying streak to 20 consecutive months (14.93 tonnes in June), providing a structural floor for demand. The overarching cross-market thread: geopolitical risk premia and structural commodity supply deficits are dominating price action while the macro regime (Fed policy, yields) remains in flux.

Data as of 11:35 am CT July 17, 2026.

WHEAT (ZWU26) — USDA HISTORIC SUPPLY SHOCK + CPC DROUGHT EXTENSION

CBOT SRW Wheat (ZWU26) is the week's standout fundamental story — a supply-driven structural breakout that is inverting the typical July harvest-pressure seasonal. With USDA forecasting the smallest U.S. winter wheat crop since 1965 and a reinforcing CPC drought outlook extending across the Great Plains through late July, the path of least resistance remains higher toward the 700¢ 52-week high and beyond.

PRICE ACTION & TECHNICAL STRUCTURE

ZWU26 as of this writing at 680.75¢, within 2.8% of its 52-week high of 700.00¢, after carving an intraday high of 683.00¢ on the session. Volume of 65,551 contracts ran at 75% of the 20-day average (87,318), confirming the move was not a thin-market spike but rather a sustained institutional repositioning.

The technicals are broadly bullish: price trades above all four key moving averages (MA20: 619¢, MA50: 627¢, MA100: 624¢, MA200: 594¢) with ADX at 34.41 and DI+ (34.41) comfortably clearing DI- (12.10) — indicating a strong, established directional trend. RSI at 70.67 is technically elevated but not yet at extremes for a structural breakout. Support established at 663.375¢ (prior pivot + 20d MA convergence zone); resistance at 692.125¢ before the 700¢ 52-week high.

FUNDAMENTAL THESIS

USDA delivered a generational supply shock: its July outlook forecasted the 2026–27 U.S. winter wheat harvest at 1.048 billion bushels — down 25% from the 2025–26 crop and the smallest yield since 1965. Hard red winter wheat (western Kansas, eastern Colorado, the Oklahoma/Texas Panhandle) was forecast at 514.8 million bushels, down 36% year-over-year as drought devastated prime growing regions. Australia compounded the global balance-sheet tightening, projecting its 2026 harvest at 9.5 million metric tons — down nearly 30% from 13.3 MMT in 2025 — removing a key export competitor from the market.

U.S. weekly export sales (week ending July 9) came in at 235,100 MT, below market expectations, signaling some near-term demand resistance at elevated prices, though export inspections for the week remained supportive.

The CPC 6–10 day outlook (valid July 18–22) calls for below-normal precipitation across the Northern and Central Great Plains, western Corn Belt, and Upper Mississippi Valley, extending drought stress and maintaining the structural supply-deficit narrative through at least late July. (Reference: https://www.cpc.ncep.noaa.gov/products/predictions/610day/index.new.php)

Seasonal Note: July–August typically carries harvest-pressure headwinds for SRW wheat as new crop supply enters commercial channels — but the pattern historically inverts in structurally short-crop years; USDA's 2026 winter wheat crop forecast puts this squarely in the inversion camp, and the current price action (near two-year high, RSI 71, ADX 34) confirms the pattern is overridden.

NOTABLE BLOCK TRADES & OPTIONS ACTIVITY

Implied volatility for ZWU26 options is running at 30.87% — elevated relative to the recent historical norm for this contract, reflecting the market's uncertainty around the USDA supply estimate and weather. Realized volatility rank at the 99.65th percentile suggests options premiums are justified but sellers of vol face structural risk given the ongoing drought catalyst.

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- USDA Crop Progress: If winter wheat harvest completes at >80% with no incremental supply downgrade, expect a sell-the-news reaction toward 655–60¢ support.

- Price closes below 663¢ (support_1): Would signal exhaustion of breakout energy; structural thesis intact but timing invalidated — re-enter on a higher-low build.

- GFS/ECMWF model divergence on Great Plains precipitation: If 8–14 day models shift wetter, the weather premium component unwinds rapidly. Monitor both model runs daily.

CRUDE OIL (CLQ26) — HORMUZ RE-ESCALATION SPIKE: TRADING THE GEOPOLITICAL PREMIUM

Crude oil (CLQ26) delivered the week's most explosive price action — a +14.9% five-session surge driven by a renewed US-Iran Strait of Hormuz confrontation. The setup is now a geopolitical risk-premium trade: the escalation is live, the OPEC+ supply overhang is structural, and the EIA inventory backdrop is mixed. The opportunity lies in managing the binary: another escalation prints into blue sky above $84, while any de-escalation signal sends CLQ26 back toward $78-79 support within hours.

PRICE ACTION & TECHNICAL STRUCTURE

CLQ26 posted a current price of $82.16 — $3.21 above yesterday's settle of $78.95 — after surging from approximately $71.49 five sessions ago (+14.9%). The Iran-escalation trigger bar on July 13 was the week's defining candle: Brent crude rose more than 4% in a single session to its highest level since June 22, dragging WTI higher in sympathy.

The technical structure is constructive near-term: RSI at 59.90 has room to extend before reaching overbought territory, and ADX at 28.0 with DI+ (28.0) clearing DI- (15.67) confirms directional momentum. CL trades above its MA100 ($82.12) and MA200 ($70.81) while testing its MA50 ($82.75) from below — that 50-day level is the key near-term pivot.

FUNDAMENTAL THESIS

US-Iran tensions over control of the Strait of Hormuz reignited on July 13, with both sides trading attacks in the critical shipping lane through which approximately 20% of global seaborne crude passes. The prior ceasefire framework (mid-June) dissolved, reigniting a geopolitical risk premium that had been steadily unwinding since April's $117 peak. On the supply side, OPEC+ confirmed an additional 188,000 bpd August quota increase, part of a cumulative +600,000 bpd expansion since April, providing a structural cap to upside. The EIA's July 15 Weekly Petroleum Status Report (data through July 10) showed a -1.69M bbl crude draw, smaller than the -2.1M bbl expected, while crude stocks at Cushing rose +430,000 bbl — a mildly bearish inventory read that the geopolitical narrative overwhelmed. EIA's July STEO revised Brent forecast to an average of $74/bbl in Q3 2026 (cut by $27/bbl from last month) before the re-escalation, underscoring that the structural supply-demand balance remains soft beneath the geopolitical overlay.

Seasonal Note: Crude oil historically benefits from modest summer driving-season demand (June–August), but 2026 geopolitical dynamics and OPEC+ supply management dominate any seasonal signal; the pattern is overridden by headline risk.

NOTABLE BLOCK TRADES & OPTIONS ACTIVITY

CL's realized volatility rank is at the 92.69th percentile, reflecting the whipsaw regime created by the conflict cycle (spike-to-ceasefire-to-spike). The paper flow leans opportunistic: institutional activity has been concentrated in near-dated call spreads targeting the $85–$90 zone (capturing the geopolitical premium), with put protection bought at $75–78 (a de-escalation hedge).

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- Iran news (primary): Any formal ceasefire announcement, safe-passage agreement, or de-escalation signal invalidates the geopolitical premium leg immediately — expect $78–79 re-test within 24 hours of any such headline.

- EIA July 22 inventory (secondary): A crude build >+2M bbl or Cushing build >+1M bbl would signal demand weakness is outrunning geopolitical premium — reduces thesis conviction to 2/5.

- OPEC+ compliance: Reports of member-state over-production relative to quota would add supply-side pressure; monitor for unofficial production data from Reuters/Platts.

GOLD (GCQ26) — $4,000 FLOOR DEFENSE: CPI MISS MEETS HAWKISH FED

Gold (GCQ26) is navigating a structural correction from its January 29, 2026, peak near $5,595, now defending the $4,000 psychological floor amid hawkish Fed signaling and rising real yields. The June CPI surprise (−0.4% MoM) provided a temporary reprieve, boosting gold back through $4,000 as rate-hike odds collapsed. The $4,000–$4,051 zone is a compression point: a FOMC-driven dovish pivot on July 29 could catalyze a move to $4,100–$4,160, while a break below $3,953 support would confirm a deeper correction toward the $3,800–$3,850 zone.

PRICE ACTION & TECHNICAL STRUCTURE

GCQ26 traded at $4,021.20 (current session) vs. a prior settle of $3,992.10, posting a +$29 intraday recovery after testing a session low of $3,963.00. The weekly picture is bearish: -2.2% over five sessions (-$90 from five-session ago level), and the technical structure is structurally challenged. GCQ26 is trading below ALL four key moving averages (MA20: $4,092; MA50: $4,344; MA100: $4,612; MA200: $4,560).

Resistance sits at $4,051.50, then the MA20 ($4,092), which has capped every rally attempt in recent sessions. ATR of $106.50 per day reflects the extreme daily ranges that have characterized gold's correction phase.

FUNDAMENTAL THESIS

Three forces are pulling gold in opposite directions.

The primary headwind: Federal Reserve Chair Kevin Warsh's hawkish signaling (signaling uncertainty about rate cuts; Cleveland Fed President Hammack sees 'little evidence current rates restrain the economy') has kept real Treasury yields elevated, raising the opportunity cost of holding non-yielding bullion.

The primary tailwind: the June CPI surprise (−0.4% MoM; core CPI 2.6% YoY vs. 2.8% prior) removed near-term rate-hike risk and revived rate-cut expectations for H2 2026, sending gold back through $4,000 post-release. A structural demand floor: China's PBOC added 14.93 tonnes in June 2026, its 20th consecutive month of buying and its largest single-month purchase since 2023, buying into the historic quarterly decline.

The World Gold Council identifies $4,000 as the current 'fair value' threshold — a break below signals a potentially deeper summer correction toward $3,940 and $3,800.

The FOMC July 28–29 meeting is the decisive catalyst: a dovish statement (hold + rate-cut hints) should send GC toward $4,100–$4,160; a hawkish hold with upward rate projections would pressure $3,953 support.

Seasonal Note: Gold historically softens in summer (July–August) as jewelry fabrication demand eases from peak Asian-market levels; Q3 patterns lean slightly bearish seasonally, though in 2026 structural central-bank demand provides a non-seasonal demand floor that partially offsets the typical seasonal softness.

NOTABLE BLOCK TRADES & OPTIONS ACTIVITY

GCQ26 volume at 95,183 ran at 71% of the 20-day average (134,294), with activity concentrated in the $3,980–$4,050 range as institutional participants build straddle positions ahead of the FOMC. The options market shows put skew at $3,900–$3,940 strikes is elevated — hedges against a break of $3,953 support — while call buying at $4,100–$4,200 represents FOMC-event positioning for a dovish pivot.

CATALYST CALENDAR — NEXT 10 DAYS

WATCH ITEMS

- Session close below $3,953 (support_1): Full bearish signal; thesis invalidated. Exits immediately. Next support at $3,800–$3,850 in a clean breakdown.

- Fed communication (pre-FOMC): Any FOMC member speech signaling a hike is 'back on the table' despite the June CPI miss would re-pressurize real yields and send gold sub-$3,980.

- US-Iran de-escalation: A ceasefire reduces the geopolitical safe-haven bid that is partially supporting gold above $4,000 — removes one of the three bullish props; re-assess conviction.

SIDELINED MARKETS

COMPLIANCE & DISCLAIMER

IMPORTANT NOTICE — PLEASE READ CAREFULLY. This publication is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any futures contract. Futures trading involves substantial risk of loss and is not appropriate for all investors; leverage can work against you as well as for you. Past performance is not indicative of future results. Per CFTC Rule 4.41, any hypothetical or simulated performance results have inherent limitations, do not represent actual trading, are prepared with the benefit of hindsight, and no representation is made that any account will achieve similar profits or losses. Specific entry, stop, and target levels are published separately in companion Tactical Trade EV Cards for qualified institutional counterparties only and are not distributed with this publication. All views are as of the publication date and subject to change without notice; the publisher and its principals may hold positions in the markets discussed. This document is confidential, intended solely for the recipient, and may not be redistributed. © 2026. All rights reserved.