Top things to watch this week

The Economic Calendar:

MONDAY: Factory Orders (9:00a CT), Total Vehicle Sales (10:30a CT)

TUESDAY: LMI Logistics Managers Index (5:00a CT), Balance of Trade (7:30a CT), Redbook (7:55a CT), S&P Global Composite PMI (8:45a CT), ISM Services Index (9:00a CT), Total Household Debt (10:00a CT), 3-Year Note Auction (12:00p CT), API Crude Oil Stock Change (3:30p CT)

WEDNESDAY: MBA Mortgage Applications (6:00a CT), EIA Petroleum Status Report (9:30a CT), 10-Year Note Auction (12:00p CT), Fed Cook Speech (1:00p CT)

THURSDAY: Jobless Claims (7:30a CT), Used Car Prices (8:00a CT), Fed Bostic Speech (9:00a CT), Wholesale Inventories (9:00a CT), Fed Musalem Speech (9:20a CT), EIA Natural Gas Report (9:30a CT), Consumer Inflation Expectations (10:00a CT), 30-Year Bond Auction (12:00p CT), Consumer Credit Change (2:00p CT), Fed Balance Sheet (3:30p CT)

FRIDAY: Baker Hughes Rig Count (12:00p CT)

Key Events:

- The summer holiday season sees many traders off the desk for the next few weeks. Expect low volume and more volatility.

- The market continues to digest the weak jobs report inflection point.

- Is it RISK OFF or BTFD?

- Economic data is light this week, with nothing of note except the ISM Services PMI.

- FOMC speakers – Cook, Musalem, and Bowman (dove).

- BOE rate announcement expected to lower by 25 basis points to 4%.

- Earnings of note on PLTR, CAT, AMD, MCD, and UBER

Summer holiday trading doldrums

The summer doldrums are here, and so is the B-team. With the A-listers off at their Hamptons getaways and Mediterranean cruises, trading desks are being manned by a skeleton crew fueled by lukewarm coffee and the faint hope of an early Friday.

Expect volumes to be as thin as a summer suit with some added volatility. Don’t be surprised if the market moves are dictated by the office intern’s rogue mouse click.

Stock seasonal pattern

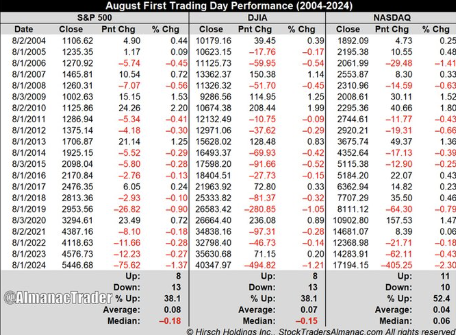

The latest data indicates this day-of-month pattern held once again.

On Friday, the S&P 500 continued its historical trend of poor performance on the first trading day of August, dropping -1.72%, a pattern that has seen the index fall in 11 of the last 15 years.

The NASDAQ has a better long-term record, rising 52.4% of the time in the previous 21 years, though it has now declined for three consecutive years on this day, including a -2.3% drop in 2024, and -2.06% now for 2025.

Seasonality for August

Seasonality for long stock positions isn’t your friend from now til mid-September, so plan your trades accordingly.

Trading the mental game

Discomfort is Your Competitive Edge

Cutting a loss feels terrible, and that’s precisely why most traders fail.

Your emotional wiring tells you to hold onto losers and cut winners because it feels safer to avoid realizing the pain. But feelings are designed to keep you alive in the wilderness, not to make you money in financial markets. When you force yourself to take that small, uncomfortable loss, you’re doing something most traders will never do—you’re choosing logic over emotion.

That sick feeling in your stomach when you hit the sell button at a loss? That’s not weakness—that’s the sound of you building the mental muscle that separates professionals from gamblers. The best traders have trained themselves to find comfort in discomfort, to see cutting losses not as failure but as proof they can do what the market demands. Every quick loss you take is practice for the discipline that will eventually make you rich.

Stock index futures

The message continues to be “Hedge When You Can, Not When You Have To.”

U.S. markets tumbled as the S&P 500 futures experienced their sharpest decline in over two months, dropping -1.6%.

The sell-off was driven by a weaker-than-expected jobs report, new U.S. tariffs, and an 8% plunge in Amazon’s share price. While the Q2 earnings season was a major focus, with positive reports from Meta Platforms and Microsoft, Amazon’s disappointing results weighed on the tech sector, while Apple’s performance was largely in line with expectations.

A tsunami of buying, fueled by flows from volatility-control strategies and record retail leverage, has pushed risk sentiment and positioning to extreme levels. This flipped on Friday’s down market.

Now, warning lights are flashing, including stretched sentiment, extreme long positioning by Commodity Trading Advisors (CTAs), seasonality risks, and a market with a scarcity of hedges.

CTA flows, which were a buying force but are described as fragile, are susceptible to flipping to a selling mode if trends break or volatility resets a little more.

In this environment, Charles McElligott of Nomura recommends outright VIX calls as a “convex hedge”. He notes that many are abandoning traditional S&P downside hedges due to their constant cost in a market with no pullbacks, making VIX calls and call spreads a more appealing hedging strategy.

Tariffs

Tariffs are here to stay.

The Trump administration has met its tariff deadline by finalizing a series of bilateral trade agreements, most notably a 15% tariff deal with the European Union. While a separate track for negotiations with China has been extended by 90 days, many other trading partners now face tariff increases of 15% or more, effective August 7th.

These new agreements, though viewed as favorable by the administration, are already facing legal challenges regarding the President’s authority and have been accompanied by new sectoral tariffs, including a 50% levy on copper, with more expected for sectors such as pharmaceuticals and semiconductors.

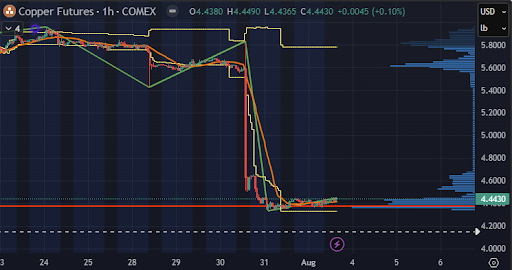

Copper futures

A new “TACO slam” from the Trump administration—a universal 50% tariff on semi-finished and copper-intensive products, a 40% tariff on Brazil, and the elimination of “de-minimis” rules—sent copper futures into a freefall.

The move, announced during a Fed press conference, caused copper futures to drop 18% instantly, with the COMEX/LME spread blowing out to over $2,600/t.

This policy-driven volatility created a “take the pop, fade the flop” trading environment, with the new tariffs expected to hit sectors like EVs, housing, and data centers despite the headline copper price drop.

Goldman Sachs subsequently withdrew its long COMEX-LME spread trade recommendation, citing the possibility of new supply deals that could mitigate the tariff impact on U.S. prices.

However, with copper now in the “bargain bin,” some analysts suggest the downturn could present a reasonable entry point for long-term players who believe in the AI growth thesis, where copper remains a vital component.

U.S. labor and employment picture

You’re FIRED!!! Trump fires labor statistics boss hours after the release of weak jobs report. I guess he did not like the numbers.

The U.S. labor market is showing significant signs of weakening, with the July Nonfarm Payrolls (NFP) report coming in far below expectations. The economy added just 73,000 jobs, missing the consensus forecast of 104,000. This disappointing headline figure was compounded by massive downward revisions to the May and June reports, which were collectively revised lower by 258,000 jobs, effectively signaling a near-halt in job growth for those months.

This weak jobs data has direct and significant implications for U.S. interest rates (see below). A labor market this soft, especially when viewed with the negative revisions, strongly supports a more dovish stance from the Federal Reserve. It undermines the case for maintaining “higher for longer” interest rates. It will likely increase market and political pressure on the FOMC to deliver earlier and more aggressive rate cuts in the coming months.

Interest rate futures

A labor market data print this soft, especially when viewed with the negative revisions, strongly supports a more dovish stance from the Federal Reserve. It undermines the case for maintaining “higher for longer” interest rates. It will likely increase market and political pressure on the FOMC to deliver earlier and more aggressive rate cuts in the coming months.

FOMC interest rate decision

The recent FOMC decision was notable not for a change in interest rates—as widely expected, the Fed held steady—but for a potential break in the committee’s traditional unity. As predicted, Governors Michelle Bowman and Christopher Waller, both Trump appointees, dissented by voting for a rate cut, a move that hasn’t seen two governors dissent since 1993. This action, rooted in their belief that the labor market is weaker than official reports suggest, publicly fractured the consensus and signaled a growing internal push for easier monetary policy.

In his commentary, Chairman Powell acknowledged the uncertainty surrounding tariffs. He stated it is “still quite early days” to fully see their impact on prices, yet he conceded that tariffs are “starting to show up in consumer prices.” Powell reinforced a cautious, data-dependent approach, emphasizing that the Fed will have to “watch and learn” on the relationship between tariffs and inflation. This “wait-and-see” stance contrasts with the dissenters’ more immediate call for action, underscoring the divide on the committee and the complexity of the current economic environment.

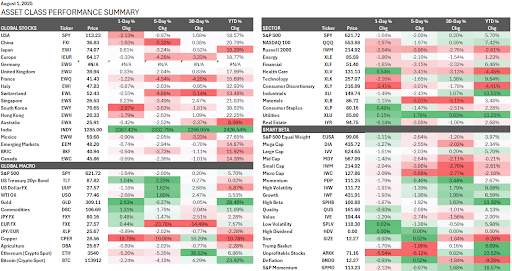

Asset class performance summary

These performance charts track the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.